The S&P 500 (^GSPC) is nearly in a bull market. But that doesn’t mean everyone is latching onto the index for a ride higher.

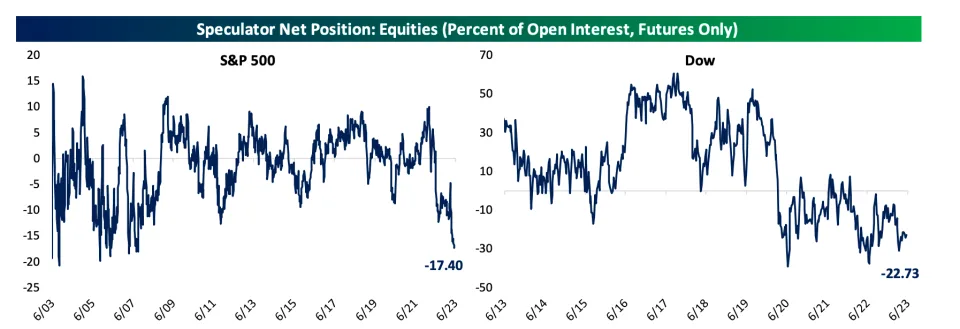

Data from CFTC’s Commitments of Traders report compiled by Bespoke shows S&P 500 futures are 17.4% short. That’s the worst reading since September 2007.

The S&P 500 hasn’t taken this long to reach a bull market off the lows since 1957-1958, per Bespoke. And the slow churn upward has strategists increasingly mixed on what comes next.

There are folks that say the breadth of the rally, or lack their of, is concerning.

“While there will undoubtedly be individual stocks that deliver accelerating growth from spending on AI this year, we do not think it will be enough to change the trajectory of the overall cyclical earnings trend in a meaningful way as top line decelerates and cost pressures remain sticky,” Morgan Stanley chief investment officer Mike Wilson wrote in a note to clients on Monday.

Strategists like Wilson point to a lagging impact of stricter Fed policy and the potential for declining earnings in the second half of the year. But there’s also a growing case for the bulls to hold strong through end of 2023.

To officially rise 20% from its October low and enter a bull market the S&P 500 needs to hit 4,292.44. Four strategists Yahoo Finance tracks closely have boosted their price target in the last week alone. The most recent of which is BMO Capital Markets chief investment strategist Brian Belski.

“Through five months of the year, it has become increasingly clear to us that stock market resilience is here to stay,” Belski wrote in a note on Monday . “Admittedly we entered the year more cautious than we have been in the past given the host of uncertainties the market faced to begin 2023, but it seems that all the doom and gloom that many others were prognosticating has yet come to fruition.”

Artificial intelligence has been the driver of the recent trend up in stocks. Nvidia (NVDA), the fourth heaviest weighted stock in the S&P 500, has seen shares soar roughly 35% in the last month after projecting higher than expected revenue in the current quarter due to AI demand. Shares of Microsoft (MSFT), Google (GOOGL) and Meta (META) have all increased handsomely this year as well. Even Tesla (TSLA), which has seen in a run in its stock price for a variety of reasons, is seen as an AI play by some.

While the run has been significant, not all of Wall Street is calling it over yet either.

“The AI hype surrounding the Tech sector is real and likely to propel future growth for many stocks within the space,” Belski wrote. “So, despite an extremely strong (year-to-date) sector performance, we believe the momentum, even if it slows a bit, is likely persist for the foreseeable future.”

Julian Emmanuel, who leads Evercore ISI’s Equity and Portfolio strategy, believes we’ve entered a “momentum market” driven by the AI surge. That means things will be volatile, per Emmanuel. Perhaps indicating those betting against the S&P 500 at a historic rate could be right after all.

Or perhaps, Emmanuel, who raised his full-year price target on the S&P 500 from 4,150 to 4,450 on Sunday, will be right come year-end. Either way, it might be a bumpy ride into the next bull market.

“Just remember to ‘check your emotions at the door,’ because it is likely to be quite a rollercoaster ride – exciting at times, terrifying at others,” Emmanuel wrote. “That’s just the way “Momentum Markets” are . And emotions are, and always will be, the biggest drag on long term investment returns.”