Stock Markets

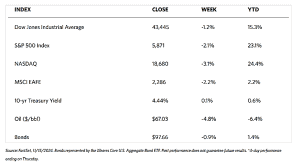

After the exuberant post-election rally, the stock market takes a breather as winning investors take profits. Major stock indexes across the board ended lower this week. The 30-stock Dow Jones Industrial Average dropped by 1.24% while the Total Stock Market fell by 2.15%. The broad S&P 500 Index lost by 2.08% and the technology-heavy Nasdaq Stock Market Composite dipped further, giving up 3.15%. The NYSE Composite lost by 1.46%. The CBOE Volatility Index (VIX), the generally accepted indicator of investor risk perception, climbed by 8.03%.

The wide dispersion of sector returns reflects the potential policy implications of the incoming administration for corporate earnings. Financials and energy shares continue to benefit from hopes for deregulation and merger approvals. Similarly, the price of Bitcoin had surged by nearly a third (32.46%) at its peak on Wednesday since the eve of the election, on investors’ anticipation of looser regulation for digital currencies. On the other hand, some healthcare shares sharply fell on Friday following the announcement on Thursday evening that Robert F. Kennedy, Jr., would be President-elect Donald Trump’s nominee as Secretary of Health and Human Services (HHS). Kennedy is a vocal critic of the pharmaceutical industry and existing public health programs, particularly vaccine initiatives. As HHS head, he would oversee Medicare, Medicaid, and other programs accounting for roughly one-quarter of government spending.

Also, notable movers during the week were electric vehicle (EV) makers, particularly Tesla. A surge in the stock price appears to have been driven by promises made by President-elect Trump that Tesla CEO Elon Musk would play a key role in his administration. At its intraday high on Monday, the stock gained 42.63% since the day before the election. Tesla and other EV makers fell back late in the week, however, when Reuters confirmed that the incoming administration plans to eliminate the $7,500 consumer tax credit for EV purchases.

U.S. Economy

The economic calendar this week was underscored by inflation data released on Wednesday. The results were largely in line with expectations. Headline prices rose by 0.2% in October and core prices (excluding food and energy) rose by 0.3%. However, year-on-year headline inflation rose for the first time since March, from 2.4% to 2.6%, due largely to stubbornly high housing costs. On Thursday, the monthly headline and core producer price inflation were released. Producer prices rose in line with expectations and their consumer counterparts.

As if to address the market expectations that rates are likely to be lowered soon. Federal Reserve Chair Jerome Powell delivered a speech on Thursday and remarked that “the economy is not sending any signals that we need to be in a hurry to lower rates,” thereby somewhat dampening sentiment. Expectations priced into futures markets for a quarter-point cut in December fell moderately over the week, from 64.6% to 58.4%. Expectations for a full percentage point of cuts by the end of the year fell further, from 41.3% to 32.6%, although it is not certain whether this was in reaction to Powell’s comments or new policy signals from the incoming administration.

Metals and Mining

Spot prices of precious metals fell for this week. Gold gave up 4.53% from its close one week ago at $2,684.77 to close this week at $2,563.25 per troy ounce. Silver ended this week at 3.32% down from its closing price last week of $31.31 to end this week at $30.27 per troy ounce. Platinum fell by 3.16% from last week’s close at $972.49 to finish this week at $941.80 per troy ounce. Palladium dropped by 3.91% from its last weekly close of $992.35 to settle this week at $953.58 per troy ounce. The three-month LME prices of industrial materials were mixed. Copper, which ended last week at $9,443.50, closed this week at $9,002.50 per metric ton, a drop of 4.67%. Aluminum, last priced at $2,620.50 one week ago, ended this week at $2,649.50 per metric ton for a gain of 1.11%. Zinc closed the previous week at $2,979.50 and this week at $2,947.50 per metric ton for a loss of 1.07%. Tin, priced last week at $31,648.00, last traded this week at $28,742.00 per metric ton for a loss of 9.18%.

Energy and Oil

The overwhelmingly bearish sentiment in the oil market was partly offset by the steep gasoline and diesel inventory draws in the United States. However, the offset was not large enough to stop the decline in oil prices. Meanwhile, China’s refinery throughput fell by 4.6% year-over-year to 14.02 million barrels per day (b/d), bearing disproportionately more heavily on independent teapot refiners in Shandong province as their utilization rate plunged to 58%, almost 20 percentage points lower than this time last year. Brent below $72 per barrel appears justified, given that China posted its seventh successive month of refinery run declines, and Jerome Powell cooled down expectations on U.S. interest rate cuts.

In other news, OPEC once more cut global oil demand growth forecasts for 2024 and 2025 for the fourth consecutive month. The projections were revised mostly by lowering China’s consumption upside to 450,000 b/d from last month’s monthly oil report, expecting 2024 demand growth to come in at 1.82 million b/d. Meanwhile, the International Energy Agency (IEA) believes that the 2025 global oil supply will exceed demand by an astounding 1 million b/d. This is equal to nearly 1% of total production worldwide, driven by the U.S., Guyana, and Canada. The IEA is keeping its demand forecast for next year unchanged at 990,000 b/d.

Natural Gas

For this report week beginning Wednesday, November 6 and ending Wednesday, November 13, 2024, the Henry Hub spot price rose by $0.30 from $1.80 per million British thermal units (MMBtu) to $2.10/MMBtu. Regarding Henry Hub futures, the price of the December 2024 NYMEX contract increased by $0.24, from $2.747/MMBtu to $2.983/MMBtu through the report week. The price of the 12-month strip averaging December 2024 through November 2025 futures contracts rose by $0.14 to $3.100/MMBtu. Natural gas spot prices rose at most locations along with the Henry Hub price this report week. Price changes ranged from a decrease of $0.72 at Northwest Sumas to an increase of $1.63 at the Waha Hub.

International natural gas futures prices increased this report week. The weekly average front-month futures prices for liquefied natural gas (LNG) cargoes in East Asia increased by $0.02 to a weekly average of $13.54/MMBtu. Natural gas futures for delivery at the Title Transfer Facility (TTF) in the Netherlands, the most liquid natural gas market in Europe, increased by $0.69 to a weekly average of $13.48/MMBtu. In the week last year corresponding to this report week (beginning November 8 to November 15, 2023), the prices were $17.17/MMBtu in East Asia and $14.97/MMBtu at the TTF.

World Markets

The pan-European STOXX Europe 600 Index ended lower by 0.69%, its fourth consecutive weekly descent. Investor sentiment is weighed on the concerns about the incoming Trump administration’s trade policies and the political upheaval in Germany. Also dampening buying incentives were cautious comments by Federal Reserve Chair Jerome Powell regarding U.S. interest rates. The major stock indexes were mixed. France’s CAC 40 Index dipped by 0.94%, Italy’s FTSE MIB climbed by 1.11%, and Germany’s DAX was mostly unchanged. The UK’s FTSE 100 Index was modestly down. Data on the Eurozone’s economy remained supportive of a soft landing. Eurostat’s second GDP estimate confirmed the surprisingly resilient 0.4% third-quarter expansion. Additionally, although Germany’s economy is expected to contract by 0.1%, the European Commission projected growth of 0.8% in 2024. Other data indicate that the labor market remained stable. In the third quarter, employment rose by 0.2%, compared to 0.1% in the preceding three months. Regarding monetary policy, the European Central Bank (ECB) policymakers unanimously approved of the quarter-point interest rate cut in October because, according to the minutes of the meeting, “the disinflationary trend was getting stronger” and there was a need to avoid “harming the real economy by more than was necessary.” The ECB also cited “prudent risk management” and provided insurance against downside risks that could lead to an undershooting of the inflation target.

Japan’s stocks lost ground over the week. The Nikkei 225 Index fell by 2.2% while the broader TOPIX Index slid by 1.1%. Providing some degree of support was the weakness of the yen since many of the listed counters generate revenues from export sales, but the uncertainties related to President-elect Donald Trump’s incoming administration raising tariffs weighed on the outlook for these same companies that heavily export to the U.S. The yen weakened to the JPY 155 range against the U.S. dollar from about JPY 152.6 at the end of the preceding week. The greenback strengthened at the back of Trump’s victory in the recent presidential election. The yen came under pressure when some fears arose that the incoming administration’s policies could prove inflationary and halt the plans of the Federal Reserve to lower borrowing costs. Another factor is the uncertainty regarding the timing of future interest rate hikes by the Bank of Japan (BoJ). Japan’s gross domestic product grew by 0.2% quarter-on-quarter during the third quarter of this year, slowing from the 0.5% increase recorded for the second quarter. The economy grew by 0.9% on an annualized basis, down from 2.2%. Increased private consumption (which accounts for more than half of the economy) drove the second consecutive quarter of GDP growth. A one-off income tax cut and higher summer bonuses also supported the GDP reading for that quarter.

Evidence of persistent deflation and worries about potential U.S. tariffs under income U.S. President Trump impacted investor confidence and brought Chinese equities lower for the week. The Shanghai Composite Index dropped by 3.52% while the blue-chip CSI 300 lost 3.29%. The Hong Kong benchmark Hang Seng Index slumped by 6.28%. Largely due to lower food and energy prices, China’s consumer price index rose by a below-consensus 0.3% in October year-on-year, down from 0.4% in September. Core inflation (which excludes volatile food and energy costs) increased by 0.2%, more than the 2.5% decrease analysts predicted and accelerating from the 2.8% drop in September, further extending the deflation in factor gate prices that commenced in late 2022. Retail sales expanded by 4.8% from a year ago which exceeded both analysts’ expectations and September’s 3.2% rise, marking the strongest growth since February. Industrial production rose by 5.3% year-on-year, lower than forecasted, and the 5.4% increase in September amid weaker auto sales. According to data from the National Bureau of Statistics, new home prices in 70 cities dropped in October by 0.5% from September, compared to home prices dropping by 0.7% from August. The October decline marked the second month of slowing home price declines and the slowest pace since March. The improvement was the result of Beijing unleashing a series of stimulus measures in recent months, which are aimed at boosting the housing sector. The measures include reducing mortgage rates, cutting taxes on home purchases, and relaxing homebuying curbs in big cities.

The Week Ahead

In the coming week, important economic releases will include the Conference Board’s leading indicators, PMI data, and the results of the Philadelphia Fed manufacturing survey.

Key Topics to Watch

- Home builder confidence index for Nov.

- Chicago Fed President Austan Goolsbee welcoming remarks (Nov. 18)

- Housing starts for Oct.

- Building permits for Oct.

- Chicago Fed President Austan Goolsbee speaks (Nov. 19)

- Fed Gov. Lisa Cooks speaks (Nov. 20)

- Fed Gov. Michelle Bowman speaks (Nov. 20)

- Initial jobless claims for Nov. 16

- Philadelphia Fed manufacturing survey

- Cleveland Fed President Beth Hammack welcoming remarks (Nov. 21)

- Existing home sales for Oct.

- Leading economic index for Oct.

- Kansas City Fed President Jeff Schmid speaks (Nov. 21)

- Fed Vice Chair for Supervision Michael Barr speaks (Nov. 21)

- S&P flash U.S. services PMI for Nov.

- S&P flash U.S. manufacturing PMI for Nov.

- Consumer sentiment (final) for Nov.

- Fed Gov. Michelle Bowman speaks (Nov. 22)

Markets Index Wrap-Up