plans now offer Roth contributions – but only 21% of workers take advantage")

Social Security is more than just a social program for many people. Nearly 90% of current retirees depend on their benefits, according to a 2023 poll from Gallup, and roughly 60% of that group say that their checks are a major source of income.

There’s nothing necessarily wrong with relying on Social Security in retirement. However, it’s important to have realistic expectations about how far your benefits will go.

The average Social Security benefit varies widely by age, but even the highest average benefit is less than you might think. Here’s exactly how much the average retiree collects at age 62, 65, 67, and 70 — as well as a few strategies to increase your benefit.

Average Social Security benefit by age

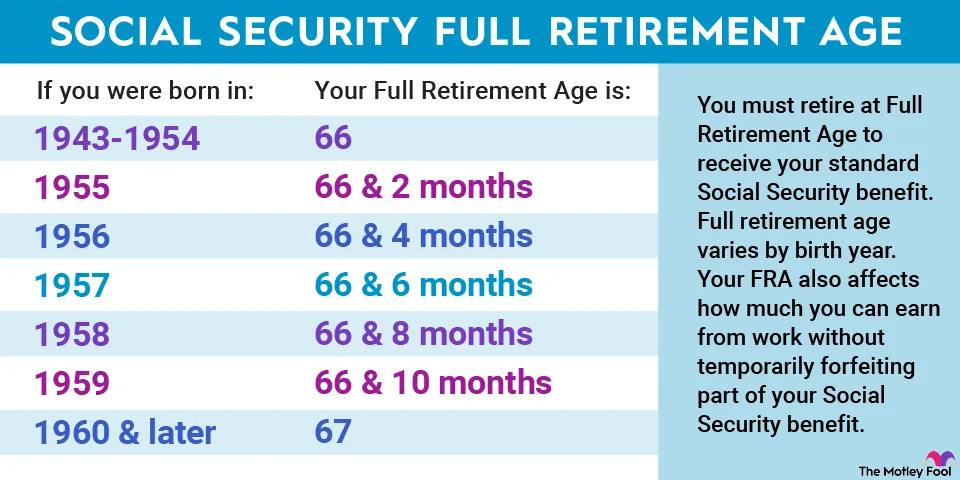

The age you begin claiming will have a major impact on the amount you receive each month. Your full retirement age (FRA) is the age at which you’ll receive 100% of the benefit you’re entitled to based on your work history. It varies by birth year, but everyone born in 1960 or later has an FRA of 67 years old.

You can file before or after your FRA, but it will affect the size of your payments. Claim as early as possible at age 62, and your benefit will be reduced by up to 30% compared to your FRA benefit amount. If you wait until age 70, you’ll receive your full benefit plus a bonus of at least 24% per month.

These adjustments are permanent, too, making it extra important to choose your claiming age wisely. If you change your mind later in life, you’re stuck with this decision.

Again, the average benefit varies based on age. Here’s how much the average retired worker collects at various ages, according to the Social Security Administration’s most recent data released in December 2023:

| Age | Average Monthly Benefit Among Retired Workers |

|---|---|

| 62 | $1,298 |

| 65 | $1,563 |

| 67 | $1,884 |

| 70 | $2,038 |

Source: Social Security Administration.

Benefits also vary between men and women. Men, on average, earn roughly $300 more per month than women at all of these ages, according to the Social Security Administration data.

While Social Security can go a long way in retirement, the average retiree may have a tough time surviving on their benefits alone. Considering that even at age 70 the average benefit is just barely above $2,000 per month, most retirees will need some other source of income to make ends meet.

Simple strategies for increasing your benefits

One of the best ways to set yourself up for a more comfortable retirement is to increase your savings, but that’s often easier said than done. Saving for retirement is tough, and as costs continue to rise, many people are already stretched thin financially.

If you’re already saving as much as you can, another option is to increase your benefit amount. A few of the simplest strategies to boost your monthly payments include:

- Delay claiming: Waiting even a year or two to file can increase your benefits by hundreds of dollars per month. Even if you can’t afford to wait until age 70 to claim, delaying as long as possible can still result in significantly larger checks each month.

- Work for a full 35 years: The Social Security Administration bases your benefit on an average of your wages throughout the 35 highest-earning years of your career. If you’ve worked for fewer than 35 years by the time you file, you’ll have zeros added to your average — which will reduce your benefit amount.

- Consider working more than 35 years: Because only your top-earning 35 years are included in your average, working for longer than 35 years can sometimes boost your benefit. Chances are you’re earning more now than you were earlier in your career, and when you have more of these higher-earning years in your average, it will result in larger checks each month.

Small steps can make a big difference in your benefit amount, and it’s simpler than it may seem to increase the size of your checks. When you have realistic expectations about how far Social Security can go, you can set yourself up for a more financially secure retirement.