plans now offer Roth contributions – but only 21% of workers take advantage")

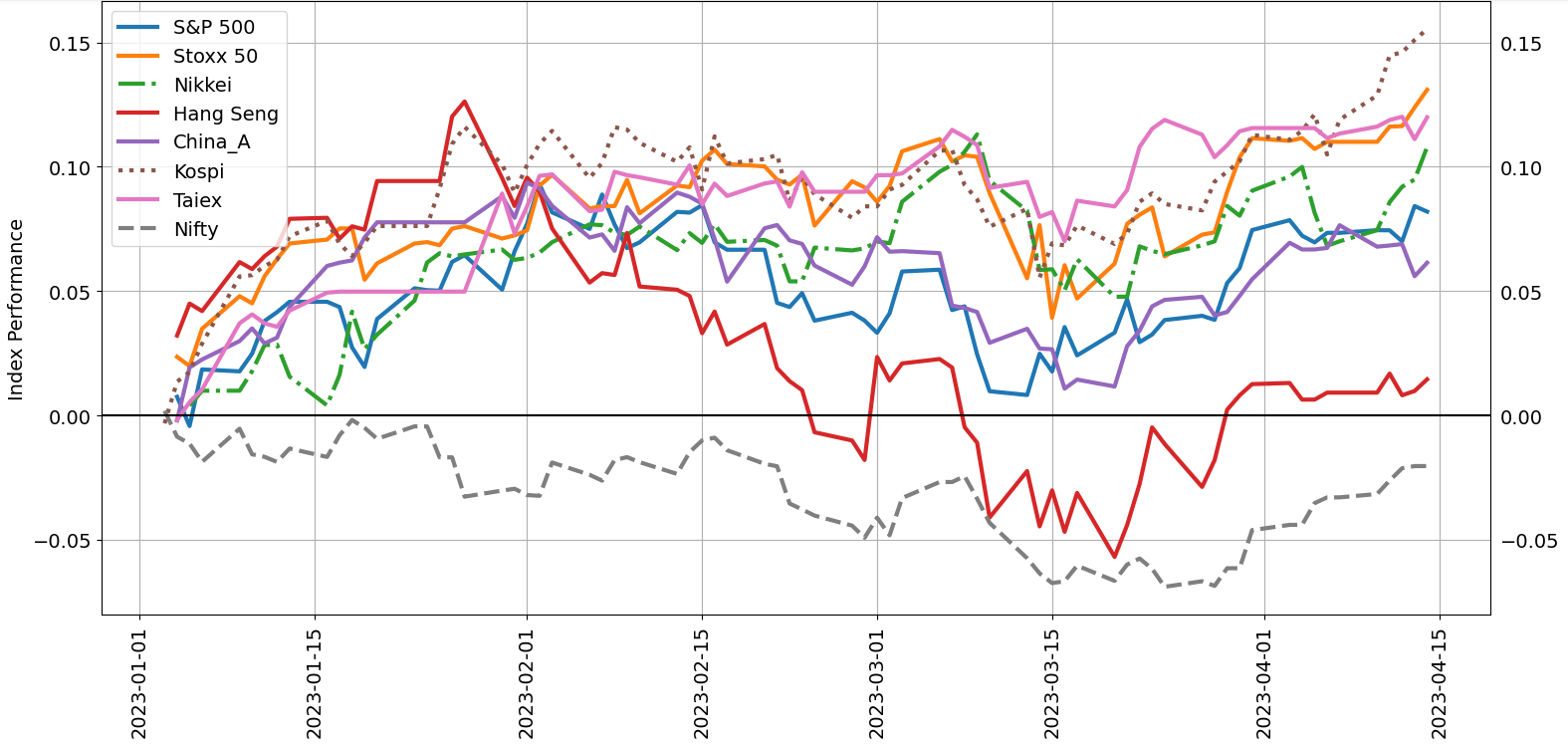

Global equity markets rose while the US dollar slipped in the past week on growing expectations that the US Federal Reserve is nearing the end of its tightening cycle. The MSCI All Country World Index rose 1.3%, and the US dollar index (DXY index) fell 0.5%. Within equities, the S&P 500 rose 0.8%, while the Nasdaq 100 index gained 0.1%. The German DAX 40 advanced 1.3% and the UK FTSE 100 jumped 1.7% respectively, while Japan’s Nikkei 225 soared 3.5% and the Hang Seng index rose 0.5%.

A subdued US CPI report on Wednesday and the unexpected decline in US producer prices cemented the view that broader price pressures are subsiding. This coupled with a forecast from Fed staff showed that banking sector stress would tip the economy into a mild recession was enough to cement the view that the Fed is nearing the end of the tightening campaign.

Minutes from the FOMC meeting in March published in the week showed several policymakers considered pausing interest rate increases, but concluded high inflation needed to be tackled. This was echoed by Richmond Fed President Thomas Barkin that price pressures are not sufficiently weak, San Francisco Fed President Mary Daly remarks on Wednesday that the Fed has “more work to do”, and Fed Governor Christopher Waller comments on Friday that the central bank’s lack of progress on bringing down inflation meant rates needed to move higher.

Year to Date Equity Market Performance

Source Data: TradingView

Data published on Thursday showed US producer prices unexpectedly declined in February, solidifying the view that broader price pressures are cooling. This follows a subdued US CPI report on Wednesday and the dovish tone of the minutes of the FOMC meeting in March, boosting hopes that the Fed is nearing the end of its current tightening cycle. Interest rate markets are pricing in about a 78% chance that the Fed will raise rates one more time by 25 basis points at its May 2-3 meeting, according to CME’s FedWatch tool.

The first-quarter US earnings season has kicked off on a strong note, according to FactSet. So far 6% of the companies in the S&P 500 have reported actual results for Q1 2023, of which 90% have reported actual EPS above estimates. The earnings season picks up steam in the coming week with several high-profile companies reporting, including Goldman Sachs, Morgan Stanley, Netflix, and Bank of America.

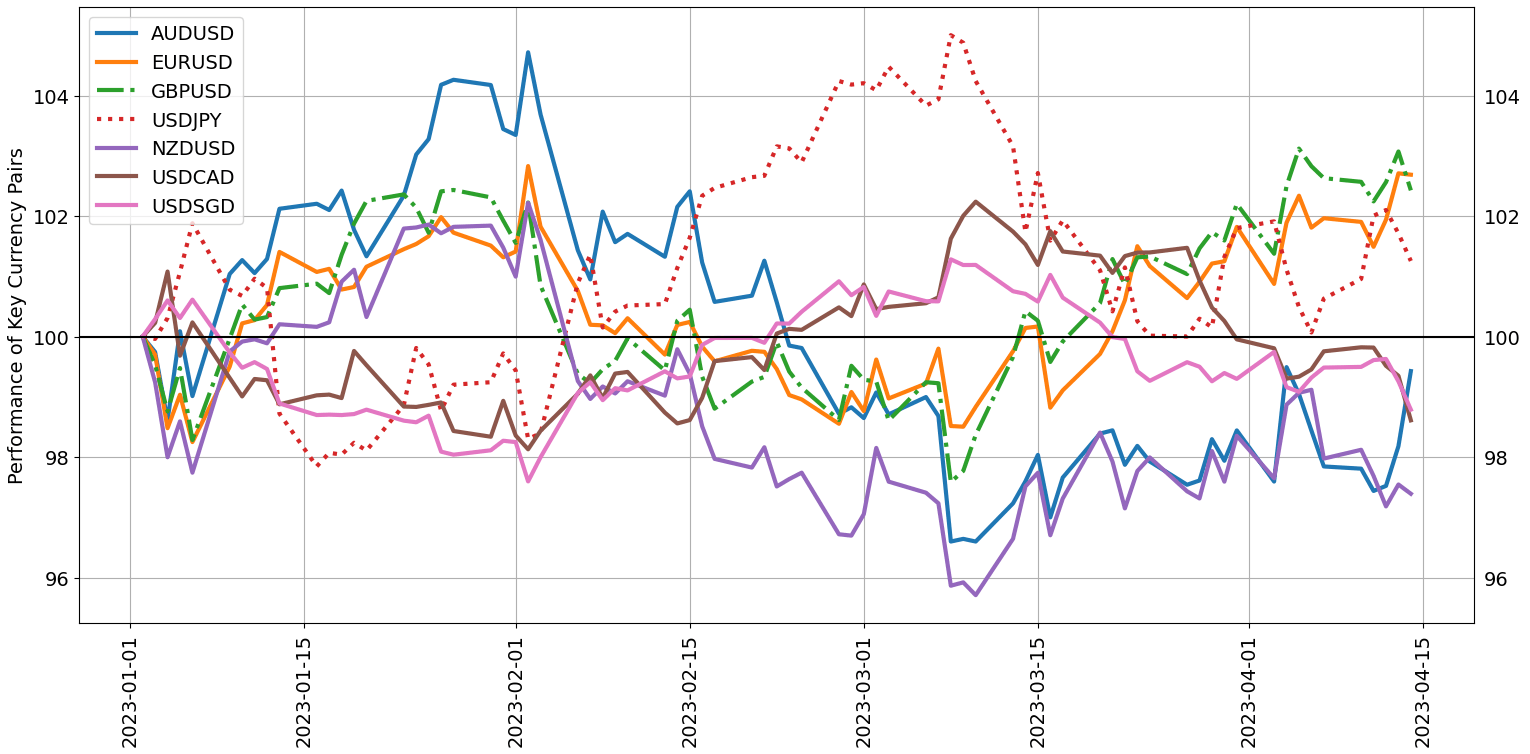

Year to Date Performance of Key Currency Pairs

Source Data: TradingView

A spate of macro data is due on Tuesday, starting with China’s Q1 GDP, and industrial production, retail sales, and fixed asset investment for March; plus, minutes of the RBA meeting, German ZEW economic sentiment for April, and Canada’s March inflation data. Euro area inflation and UK inflation data for March are due on Wednesday, and New Zealand inflation data for Q1, and the ECB monetary policy meeting accounts will be released on Thursday. Japan’s inflation data for March is due on Friday.