You’re not imagining it. Things don’t merely seem more expensive these days — consumer prices are actually accelerating at their fastest pace in 13 years. This higher inflation doesn’t just affect the price you pay at the register. It can also have an impact on your major purchases, investments, and more. And for communities of color and the income-constrained, that impact may be magnified due to higher levels of debt and structural unemployment, both of which may make the experience of inflation more challenging. Here’s how inflation may affect you and what you can do about it.

According to financial expert and CEO of Torch Enterprises, Dr. Pamela Jolly, while the impacts of inflation may be felt across all income levels, “People who are either income constrained or have inconsistent income streams will feel the most impact.”

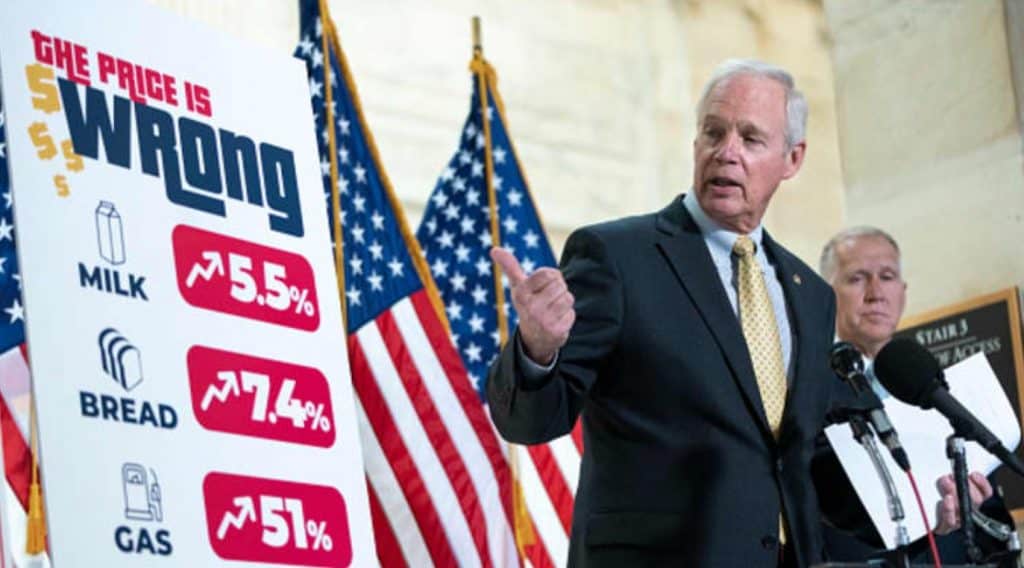

Though the overall Consumer Price Index rose by 5% year-on-year in its latest reading, not all consumer goods accelerated at the same pace. The greatest price increases were concentrated in energy, commodities, and transportation (gasoline, for example, rose 56% over the past year, while used cars and trucks were up nearly 30%). That means, that at least in some cases, savvy consumers can take certain steps to minimize the impact of inflation on their pocketbooks.

Here are a few alternatives for avoiding the most significant impacts of inflation on your purchases.

Food inflation

While food outside of the home has seen average price increases of 4%, food inside the home has increased by a more modest 0.7% year-on-year. Choosing to eat at home has always been more economical, but current inflation rates further underscore this. Furthermore, meat, poultry, fish and eggs have seen some of the most substantial price increases, so limiting purchases of these may lead to modest savings.

Auto and gas inflation

While the price of new vehicles increased by 3.3% over the past year, used cars have increased by nearly 30%. Given relatively low interest rates, and depending upon your particular financial circumstances, you may be able to secure better deals on new vehicles presently. But gas prices have also increased a whopping 56% (due, in part, to the Colonial Pipeline attack, whose impact on prices was transitory), and transportation services are up by 11%. So, in general, expect driving and flying to cost more these days.

Home furnishings vs. health care inflation

Comparing costs for health care and home furnishings is apples and oranges, but it does present an illustrative example of the uneven nature of inflation. Home furnishings rose by 1.9%, the largest increase in many years; similarly, costs for domestic services also increased substantially.

On the other hand, health-care costs actually decreased slightly or held steady. That means the better bang for your buck – if given the choice – may be catching up on overdue health care, rather than home maintenance or décor.

Longer-term inflation impact

The question of whether this bout of inflation is transitory and linked to the subsiding Covid pandemic, or structural and longer-lived weighs on many economists’ minds, and was weighing on the market this week as the Dow Jones Industrial Average had its worst week since January.

Dr. Jolly believes these are unusual times which call for serious reflection on our financial choices.

“We are entering a period where wealth building requires everyone to become more strategic about their financial lives — from consumption levels to building sustainable pathways beyond retirement that include savings and investment. This uncharted territory is fertile ground for both the financial industry and our most vulnerable communities.”

Jolly says Americans should keep abreast of their investments, understand debt management strategies better, and otherwise improve their financial literacy to manage their financial futures through this inflationary period. For example, if interest rates rise, home ownership may become more expensive. Credit card rates may also rise. Servicing debt or making mortgage or rent payments may become more onerous if wages don’t rise in tandem.

For that reason, Jolly advises doing everything in your power to equip yourself to manage these fluctuations, including forging stronger relationships with your banks or financial institutions. This is especially vital for communities of color. As the Covid economy taught us, people of color were more vulnerable to that financial shock in part because of fewer community banking relationships. Forging those relationships now can help less-advantaged communities withstand the impact of inflation, too.