Workers are getting higher wages, but at some point that could bite into companies’ profits.

As the economy reopens, costs are climbing for everything from packaging and raw materials to shipping. In addition to these expenses, companies are also paying more to get workers to come in the door.

But the disparity between labor costs and profits has been so wide for so long, that employers should be able to increase pay if they can raise prices for goods and services or improve productivity.

McDonald’s said last week that it was boosting wages for the 36,500 hourly workers at company-owned stores by 10%, and Chipotle announced it will raise wages to an average of $15 an hour by the end of June. Bank of America said it would raise minimum wages for its hourly workers to $25 an hour, from the current $20, by 2025.

Sports equipment company Under Armour also announced it would boost the minimum hourly wage for its retail and distribution workers to $15 from $10.

“It’s some of the strongest wage growth we’ve seen in a quarter century,” said Mark Zandi, Moody’s Analytics chief economist. He said the 3% wage growth for private workers in the first quarter was the strongest since the 1990s and productivity has picked up at the same time.

“All the anecdotes we were getting in the last few months would suggest it’s continuing,” he said.

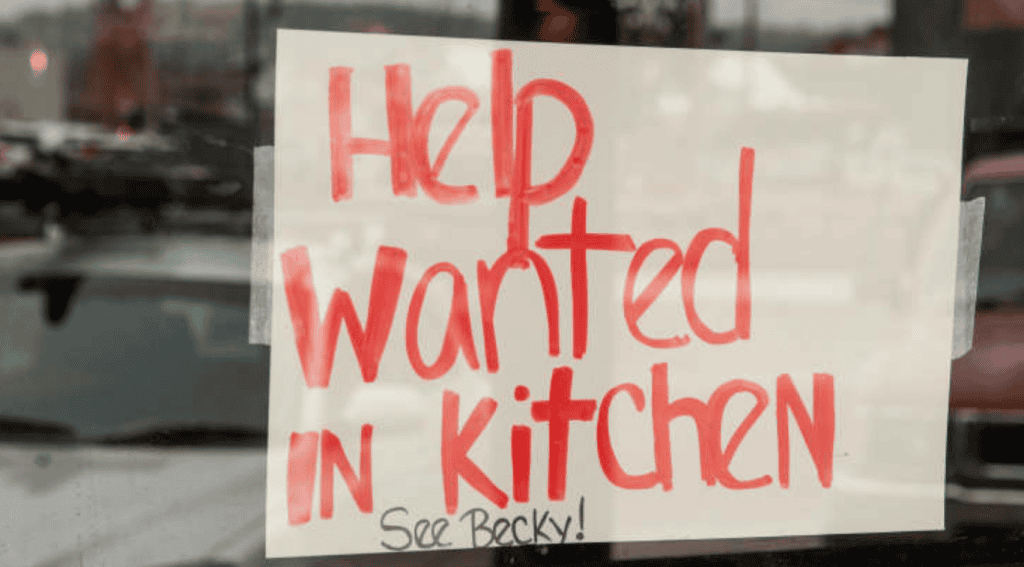

Attracting talent in a shortage

Employers are trying to address a labor shortage, according to Jonathan Golub, chief U.S. equity strategist at Credit Suisse.

“The economy is overheating and companies, even though we have a high unemployment rate, cannot get the labor they need to meet demand and they are being forced to raise wages,” he said. “It’s happening with financial services. It’s happening in industry. It’s happening in retail. You’re seeing it everywhere.”

Golub said investors are right to wonder when the higher wage costs could pressure profit margins, but he does not anticipate it becoming a problem in the near term.

“If you are seeing these pressures in an environment where the economy was weaker, this would be a disaster, but we’re not,” he said. “We’re seeing it in an environment where companies have massive pricing power, which means they can pass it on.”

But Sam Stovall, chief investment strategist at CFRA, said higher wages is one reason he has become neutral on the consumer discretionary sector, which includes retail and restaurants. The sector is up just 4.1% so far this year. It’s among the poorest performing sectors, and it’s lagging the S&P 500.

“We lowered our outlook on consumer discretionary because it is so payroll dependent,” Stovall said, noting the sector is also facing rising costs in many other areas. “The economists are calling for a 3% gain in wages in the second half of the year and a continued gain next year.”

Golub said it’s not clear how long companies will raise wages, but if it continues and becomes inflationary, it will be a problem for earnings.

“If this represents a trend where people begin to expect higher wages and they demand higher wages, and there’s a continuation, yes it becomes a problem,” he said. “We don’t know if this is a one-time adjustment.”

The “stickiness” of higher wages

Unlike temporary increases in raw materials or goods impacted by bottlenecks in the supply chain, labor costs remain on a company’s balance sheet.

“The context is super important,” said Credit Suisse’s Golub. “We know when the stimulus goes away, and the economy is no longer super-charged, and the price of lumber and gasoline comes down, the people who got higher wages are still going to have higher wages. Wages are sticky.”

Golub said wages are not a profitability problem in the near term, and the market is focused on the reopening trade now, not so much margins.

“It’s not guaranteed this becomes as margin problem, but it represents a legitimate threat to margins,” he said.

“Markets respond to things like that and they should,” Golub added. “You can see this is not by accident but the administration and others have highlighted that they want labor to get a larger share of the economy.”

Golub said he’s recommending investors invest in cyclical sectors, which include industrials, materials and financials. These companies have strong demand and pricing power. “I think it’s game on for cyclical stocks,” he said.

Stress in the system

Economists said the worker shortage showed up April’s disappointing employment report. Just 266,000 jobs were added, about a quarter of what economists expected.

Stronger gains are expected in coming months. Some economists expect more workers to show up in September when children return to school, and also when extended unemployment benefits expire.

“Right now, you’re seeing more urgent increases in wages because of the labor shortages,” said Moody’s Zandi. “Things will settle down probably toward the fall as the supply side of the economy catches up and people get back to work and we’re on the other side of the pandemic.”

Longer term, labor could remain tight even as the U.S. gets back to full employment.

“It’s not a big deal this year, probably not next year, but as you move into 2023 or 2024, wages become more of an issue. Wage pressures will intensify and take a bigger bite out of corporate profits,” Zandi said. “Companies will try to raise prices.”

The ratio of total compensation of employees to corporate profits has fallen steady from its peak of over eight times in the early 1980s to closer to five times, Zandi noted. That means the share of national income going to workers has fallen and it has stayed low as companies became more profitable.

“Compared to what has happened historically since World War II, businesses are getting a very high share of the economic pie, not as high as it’s ever been, but it’s high,” he said. “Big companies are very profitable.”

“The labor share has been very depressed…If everything sticks roughly to script, it should start to rise,” he said. “One of the new administration’s policies, where they’re working very hard, is to direct government support to low- and middle-income households.”

But Zandi said companies are likely to invest in automation, even in the service sector. “They are going to increasingly invest in labor-saving technology which they didn’t do in past decades because labor was cheap,” he said.

Mike Englund, chief economist at Action Economics, said the large 6.1% jump in personal income last year was due in part to the boost from fiscal stimulus payments, which will continue to lift income this year. He also expects employees to see higher wages, but by next year income could be flat.

That 6.1% gain in income came as corporate profits fell 5.8% last year, he noted.

Englund said the pandemic has resulted in some permanent changes in employment. “We probably downsized the restaurant industry,” he said. Englund said the industry will likely shrink in cities like New York, but it could grow in suburbs since many restaurants added takeout.

One result of the pandemic is that people moved out of cities or to different regions. “With this shift… we’re seeing shortages, a mismatch,” he said.