s — here’s the average savings rate")

Super Catch-Ups: Are They Right for You?")

If You Have $500,000 in Your Retirement Account?")

millionaires jumps 400%: Here’s what it takes to reach seven-figure status")

The biggest legislative changes to America’s retirement system in 13 years are on their way.

On Thursday, the U.S. Senate approved a spending bill that includes the bipartisan Secure Act, which aims to increase the ranks of retirement savers and the amount they put away. The measure — which passed the House earlier this week — now will head to President Trump, who is expected to sign it into law.

“The Secure Act has been years in the making,” said Paul Richman, chief government and political affairs officer at the Insured Retirement Institute. “It’s filled with common-sense measures to strengthen retirement security for millions more American workers.”

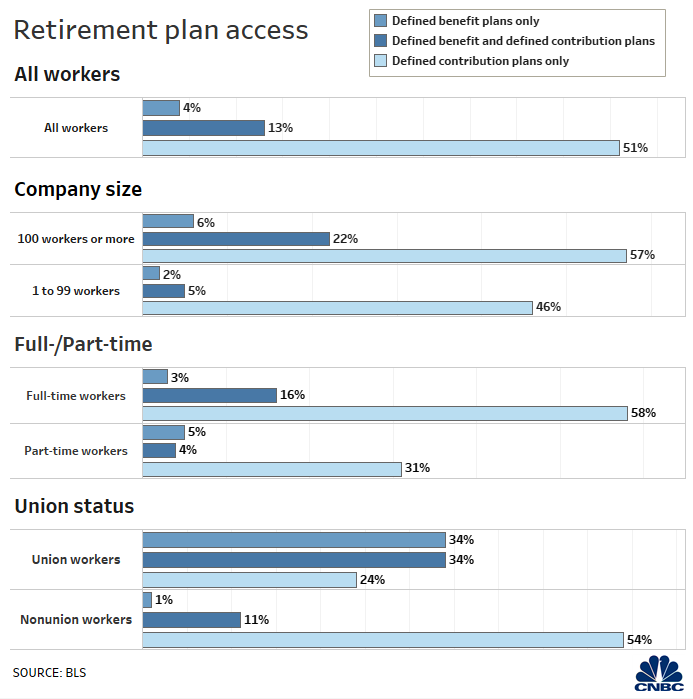

Changes include making it easier for small businesses to band together to offer 401(k) plans and offering tax credits to those firms that do; requiring businesses to let long-term, part-time workers become eligible for retirement benefits; and repealing the maximum age for making contributions to traditional individual retirement accounts (right now, that’s 70½).

It also would raise the age when required minimum distributions, or RMDs, from certain retirement accounts must start to 72, up from 70½.

Additionally, the measure aims to allow more annuities in 401(k) plans by eliminating companies’ fear of legal liability if the annuity provider fails or otherwise doesn’t deliver. While companies already can offer annuities in their 401(k) lineups, just 9% do, according to the Plan Sponsor Council of America.

Other changes include allowing money in 529 college savings plans to go toward student-loan debt (with a $10,000 limit) and letting workers with 401(k) plans withdraw up to $5,000 from their account, penalty-free, to cover the cost of having a baby or adoption.

The provisions generally are funded by modifying the rules governing inherited retirement accounts, a move expected to generate $15.7 billion over 10 years in additional tax revenue, according to an estimate from the Congressional Budget Office. Instead of being able to take required withdrawals over the course of their life as they can now, most non-spouse beneficiaries would need to withdraw the money within 10 years of the original account owner’s death.

“That’s obviously a negative for inherited traditional IRAs and for Roth IRAs that used to stretch over the beneficiary’s lifetime,” said certified financial planner Mike Hennessy, founder and CEO of Harbor Crest Wealth Advisors in Fort Lauderdale, Florida.

Meanwhile, the legislation comes as experts warn that many Americans are falling short with their retirement savings. For example, among pre-retirees ages 55 to 64, the median 401(k) account balance — half are above, half are below — is $61,700, according to Vanguard’s 2019 How America Saves Report. For those ages 45 to 54, it’s $40,200.

Additionally, roughly a third (38%) of U.S. adults say they have never had a retirement account, according to a recent Bankrate.com survey. It was most pronounced among Gen Xers (36%) and households with annual income below the $30,000 mark (58%).

Super Catch-Ups: Are They Right for You?")

If You Have $500,000 in Your Retirement Account?")