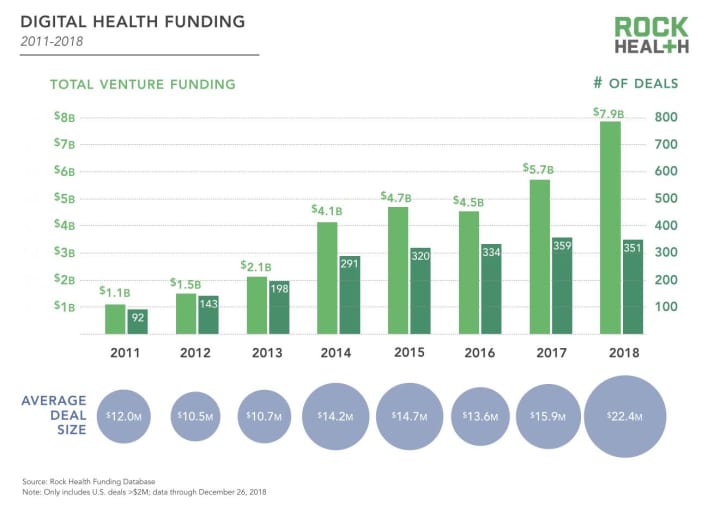

Since my company, Rock Health, began researching and tracking funding into the digital health space in 2011, we’ve reported steady growth nearly every year. 2018 was no different, with a massive $7.9 billion in venture filling start-ups’ coffers. But the signals we’re seeing — large, late-stage rounds at high valuations and shorter periods between early rounds — are those of an investment cycle nearing its peak.

Does this peak signal a “bubble?” The so-called b-word has been sneaking into conversations with our fellow investors, so we dedicated our year-end number crunching to measuring the froth.

In our view, digital health is not in a bubble. But we’ve heard opposing views on that from other investors, and so we welcome a healthy debate as this cycle unfolds.Will investors keep backing digital health?

Digital health funding from 2011 to 2018Rock Health

Future venture capital funding for digital health largely rests on two factors: the health of the economy as a whole, and the dynamics driving investment in health care innovation.

First, where the broader venture capital market goes, digital health will go. Digital health’s growth over the past five years mirrors venture investment growth overall: Both hit decade-high deal values in 2018.

But of course, the ongoing public market pullback could trigger investor wariness that spills into venture capital.

For the second factor, we validated a simple framework with fellow investors to assess the current “bubbliness” of digital health against six attributes. We hope this approach moves the bubble discussion to a more data-driven place and helps entrepreneurs identify strategies to weather a potentially tighter capital market.

Is digital health in a bubble? Maybe.Rock Health

- Hype supersedes business fundamentals: Technology’s potential to fundamentally transform the $3.5 trillion healthcare market drives excitement for digital health, not irrational hype. While startups must overcome long sales cycles and byzantine reimbursement models, investors and entrepreneurs are actively learning and moving toward sustainable business models: risking payment on clinical outcomes and pursuing strong validation pathways for reimbursement. Verdict: not bubbly.

- High cash burn rates: This is perhaps the “bubbliest” attribute of digital health—many well-funded startups are raising cash quickly. A median Series A, or first institutional, round of funding increased by a third in recent years, and since 2011, time to raise between seed and that Series A has been cut roughly in half. Savvy entrepreneurs will find ways to reduce the need for fresh capital while reaching growth milestones. As Kaiser Permanente Ventures’ Liz Rockett pointed out to us, “With sales cycles being as long as they are, you have to burn a fair amount of capital without a known endpoint to figure out where you’re headed. The CEOs who figure out how to do that as efficiently as possible will be able to retain a lot more ownership in their companies and give themselves more flexibility at exit.” Verdict: moderately bubbly.

- Unclear exit pathways: M&A for digital health companies has been flat for the past few years, and there hasn’t been an IPO since 2016. Over half of acquirers in 2018 were digital health companies themselves, primarily looking to acquire for scale and to build out their offerings. Incumbent shake-ups and the entry of tech giants will drive more demand for innovation—and opportunities for consolidation. Verdict: moderately bubbly.

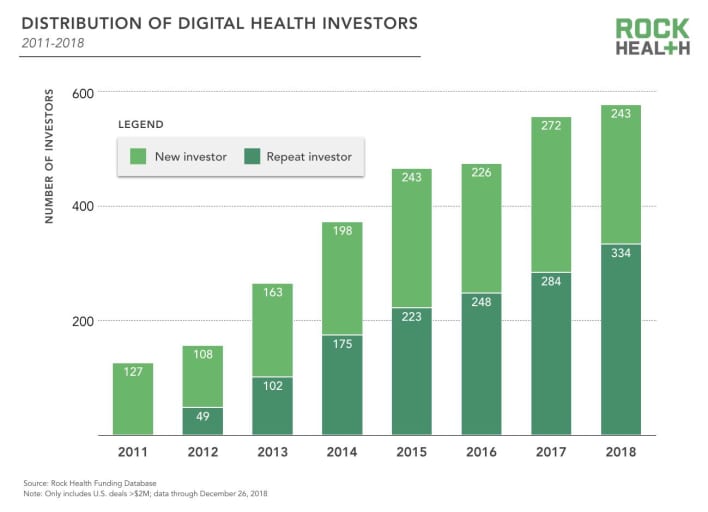

- Surge of cash from new investors: Our data shows repeat investors have outnumbered new investors for the past four years, and the spread is growing. Commitment from those who know the space well is a good sign—particularly as they encourage companies to pace growth and develop a long-term fundraising plan that doesn’t hinge on an annual influx of cash. Verdict: not bubbly.

- High valuations decoupled from fundamentals: With bigger, more frequent rounds, some valuations are soaring. Bessemer Venture Partners’ Steve Kraus cautions, “I’m not a big fan of the obsession with unicorn valuations. The focus should be on building a ‘unicorn product’ in healthcare and then the rest will take care of itself.” He sees startups hiking up valuations via large investments rather than taking a measured approach of raising less cash and selling at a lower, but good, multiple. Fortunately, this isn’t an inevitability—startups can avoid overvaluation by taking smart, not big, money. Verdict: moderately bubbly.

- Fraud or misuse of funds: Before it pops, a bubble can tempt market participants with massive returns and lead to fraud. Could Outcome Health and Theranos be indicative of a wider trend in health tech? We don’t think so. There hasn’t been further evidence of fraudulent behavior infecting the sector. Verdict: Not bubbly.

Rock Health’s data on the distribution of digital health investorsRock Health

While the future is not yet written, it seems unlikely that capital will continue to flow at the current rate. We anticipate a possible pullback in VC funding for digital health in future periods—not a bubble pop. The next stage will be shaped by how entrepreneurs and investors reset for a tighter market in 2019. Doing so will safeguard against future market corrections—and allow the digital health community to continue making healthcare massively better for every human being.