Clock Is Ticking Louder on a Stock Rally the Pros Never Believed In

News Team

The buying binge that has propelled US equities almost without interruption for four months is nearing a point where past rebounds caved in.

It’s in the charts, with the S&P 500’s recovery reaching the same half-way-point threshold that spelled doom for bulls in August. The week also featured the year’s first big blow to a dip-buying strategy that by one measure has been as strong as any year since 1928. And warnings are blaring from bonds, whose bullish thrust had given cover to equity faithful convinced they’d weathered the worst the Federal Reserve had to give.

Signs of disenchantment were also visible a week earlier among hedge funds, whose trimming of positions was the biggest in two years, according to Goldman Sachs Group Inc. data. The S&P 500 dropped 1.1% in the past five days for the worst week since mid-December.

While one bad stretch doesn’t prove anything, it highlights the riskiness of a runup that has inflated equity prices by $5 trillion at a time when central bankers say their inflation-fighting campaign may have years to go and data on earnings and the economy continue to crater. Buying stocks now means taking a flier on valuations that are high by most historical standards and betting against a pundit class that is united as it ever has been in the view that stocks are due for a reckoning.

“The first half of the year is likely to show the impact of rate hikes that began all the way back in early 2022, that are finally feeding through the economy,” said Tom Hainlin, national investment strategist at US Bank Wealth Management. “We would not have a lot of confidence that this rally that we’ve seen in early 2023 is sustainable until we see the impact of rate hikes on the real economy.”

Underpinning losses in the week were worries that the Fed may raise interest rates above 5%, potentially to 6%, to slow demand. The two-year Treasury yield jumped more than 20 basis points to above 4.50%, the biggest weekly increase since November.

The spirited equity buying came to a halt ahead of January’s consumer price index, due Tuesday, which will shed light on the Fed’s progress in its battle to curb inflation. US equity funds saw outflows of $7.7 billion in the week through Feb. 8, according to a note from Bank of America Corp. that cited EPFR Global data.

Stocks were off to a solid start this year, bolstered by signs of softening inflation and better-than-feared fourth-quarter earnings. That flew in the face of all bear warnings that a tough first half was in store. Meme stocks got a boost as day traders returned, while risky shares, such as unprofitable technology firms, jumped, likely fueled by a forced covering by short sellers. Despite lackluster profits at large-cap companies, a flurry of job cuts sparked rallies in shares like Walt Disney Co. and Meta Platforms Inc.

At the beginning of this month, almost 80% of S&P 500 stocks were trading above their 200-day moving averages. Such market breadth, among other things, sparked calls that a new bull market had begun.

Partly propelled by a retail crowd whose post-pandemic dip-buying strategy proved successful, the new-year bounce has mostly been punctuated by a big impetus to go bargain hunting. In fact, the S&P 500 has risen an average of 0.45% on the day after a fall, a stronger rebound than any year since 1928.

“The dip-buying mentality is driven by the idea that as economic growth slows, the Fed will be forced to reverse its policy approach,” said Lauren Goodwin, economist and portfolio strategist at New York Life Investments. “The buy-the-dip story is one that I actually don’t expect to prevail or to be successful when interest rates are still in restrictive territory.”

When forces such as short covering or retail exuberance are at play, placing trust in charts can be dangerous. Consider the renowned 50% retracement indicator that is often touted as a nearly foolproof signal that a rally has legs. At a closing high of 4,180 on Feb. 2, the S&P 500 erased half of its peak-to-trough decline incurred during the last year. Then it fell in four of the following six sessions.

If the pullback continues, it’d mark the second time in a year when the indicator failed to live up to its billing. A similar signal was flashed in mid-August, spurring hope the worst was over. Then the selloff renewed and stocks spiraled to fresh lows two months later.

In many ways, the rally that lifted the S&P 500 as much as 17% from its October trough has been at odds with a worsening fundamental story. Outside the labor market, the economy has weakened, as evidenced by data on retail sales and manufacturing. The recession warning in the bond market is growing louder, with the yield gap between two-year and 10-year Treasuries reaching the deepest inversion in four decades.

Moreover, analysts’ estimates on how much corporate America will earn in 2023 have kept falling. Since the end of October, expected profits have dropped 5% to $220.70 a share, data compiled by Bloomberg Intelligence show.

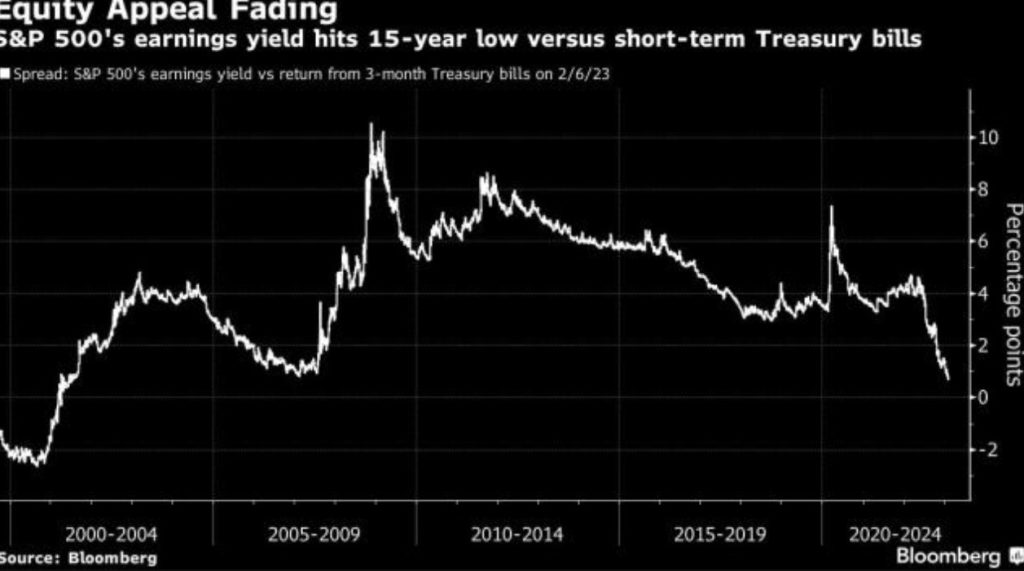

Souring earnings sentiment can be trouble in a market when stocks are already expensive. At 18.3 times profits, the S&P 500’s multiple is above its 10-year average. When stacked against cash, now earning the most in years after the Fed’s rate hikes, the index’s earnings yield has fallen to the lowest level in 15 years.

While the latest bounce was a headache for money managers who were largely defensively positioned, there are signs that few are willing to embrace the rally. In fact, hedge funds tracked by Goldman’s prime brokerage last week trimmed their long holdings as stocks went up.

“I don’t think valuations support a further run here,” said Jake Schurmeier, portfolio manager at Harbor Capital Advisors. “And I would take the retail enthusiasm as a sign of some exuberance coming back into the market, which the Fed I think is also going to look at as a bit worrying if the economic fundamentals don’t continue to support that.”