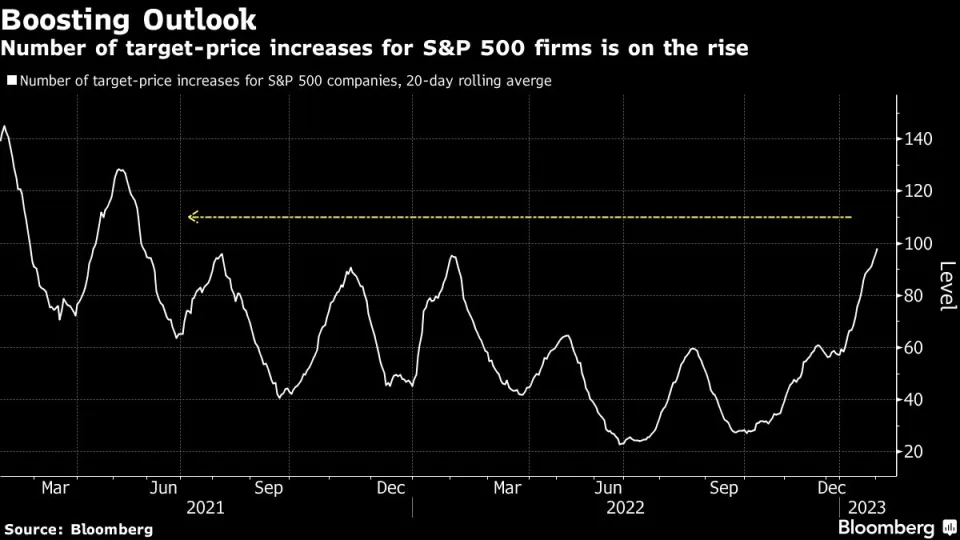

The profit outlook for companies in the S&P 500 Index is rapidly deteriorating — yet analysts can’t raise their stock-price targets fast enough.

Consider it the stock-market disconnect of 2023.

The two seemingly incompatible trends reflect how much equity prices are being driven by speculation that the Federal Reserve is nearing the end of its most aggressive rate-hiking cycle in decades. That particularly bodes well for the valuations of growth and tech stocks, which have held on to this week’s big gains even after disappointing earnings reports from Apple Inc., Alphabet Inc. and Amazon.com Inc.

But the degree to which analysts are raising stock-price targets while slashing the earnings estimates is puzzling for those used to seeing the market hinge on the underlying strength of corporate America.

“Interest rates have come down and your discount rate has come down, so even though your earnings aren’t going up, you could assign a higher price [on the stock] just because of the lower discount rate,” said Crit Thomas, global market strategist at Touchstone Investments. “They’re saying, ‘Hey, we’re going to be out of this within six to 12 months, so let’s just look through it.”

Fourth-quarter reporting season has done little to support optimism about the fundamentals. Earnings in sectors from energy to consumer discretionary have been coming in below pre-season estimates and companies are dialing back outlooks based on expectations growth will slow. In fact, Bloomberg Intelligence’s model shows that such earnings guidance for the first quarter has been cut by the most since at least 2010.

That’s forced analysts who stuck to rosier estimates to follow. Among all changes analysts made to their earnings projections last month, just 37% were upgrades, data compiled by Citigroup Inc. show. The level has been associated with the past three economic recessions and is 30% below a historical average.

“To us, 2023 analyst numbers looked too aggressive,” Drew Pettit, director of ETF analysis and strategy at Citigroup, said in an email. They are “quickly getting revised down to better match the economic reality.”

There remains considerable uncertainty about the direction of the economy, especially with Friday’s rapid job growth numbers suggesting it’s still expanding at a solid pace. Overall, however, economists broadly expect growth to slow or even contract due to tighter financial conditions.

Read more: Stock-Market Vigilantes Dial Back Penalties for Earnings Misses

“We’re starting to see some of these companies come out and give less than ideal guidance on growth,” said Brian Jankowski, senior investment analyst at Fort Pitt Capital Group. “We’re starting to see those business forecasts for growth line up better with GDP, which is predicted to be very little to flat.”

That has largely been brushed aside in the stock market by speculation that interest rates are nearing their peaks of the cycle, a view that was supported by the Fed’s decision Wednesday to dial back the pace of its move. Sell-side analysts who cover the S&P 500 companies — and already skew bullish — have responded by raising their share-price estimates at the fastest pace since the spring of 2021.

The Fed’s central role in the outlook for equity prices was underscored by how well the market performed this week in the face of some negative earnings surprises from major companies.

Apple reported a steeper sales decline in its holiday period than Wall Street expected, while Ford Motor Co. posted a profit miss amid a continuing supply shortage. Google parent Alphabet’s results signaled a lower demand for its search advertising during a slowing economy.

Yet on Friday major stock indexes were little changed for much of the day before closing lower. Even so, the S&P 500 notched its second straight weekly gain.