Workers who are nearing age 65 and have health insurance through their job may want to consider how Medicare could factor into their medical coverage.

While not everyone must sign up for Medicare at that age of eligibility, many are required to enroll — or otherwise face lifelong late-enrollment penalties.

“The biggest mistake … is to assume that you don’t need Medicare and to miss enrolling in it when you should have,” said Danielle Roberts, co-founder of insurance firm Boomer Benefits.

Roughly 10 million workers are in the 65-and-older crowd, or 17.9% of that age group, according to the Bureau of Labor Statistics.

The general rule for Medicare signup is that unless you meet an exception, you get a seven-month enrollment window that starts three months before your 65th birthday month and ends three months after it.

Having qualifying insurance through your employer is one of those exceptions. Here’s what to know.

The basics

Original, or basic, Medicare consists of Part A (hospital coverage) and Part B (outpatient care coverage).

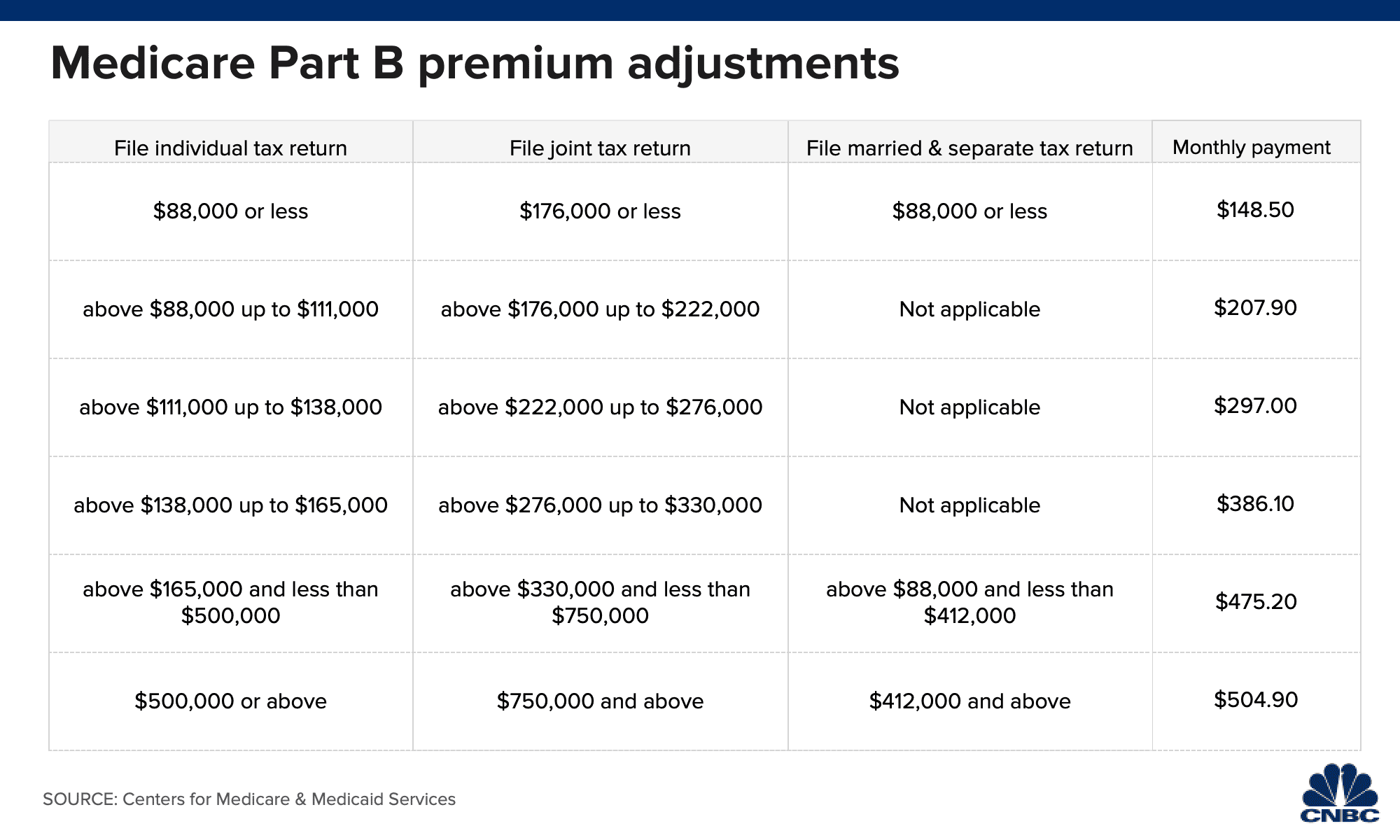

Part A has no premium as long as you have at least a 10-year work history of contributing to the program through payroll (or self-employment) taxes. Part B comes with a standard monthly premium of $148.50 for 2021, although higher-income beneficiaries pay more through monthly adjustments (see chart below).

Some 43% of individuals choose to get their Parts A and B benefits delivered through an Advantage Plan (Part C), which typically includes prescription drugs (Part D) and may or may not have a premium.

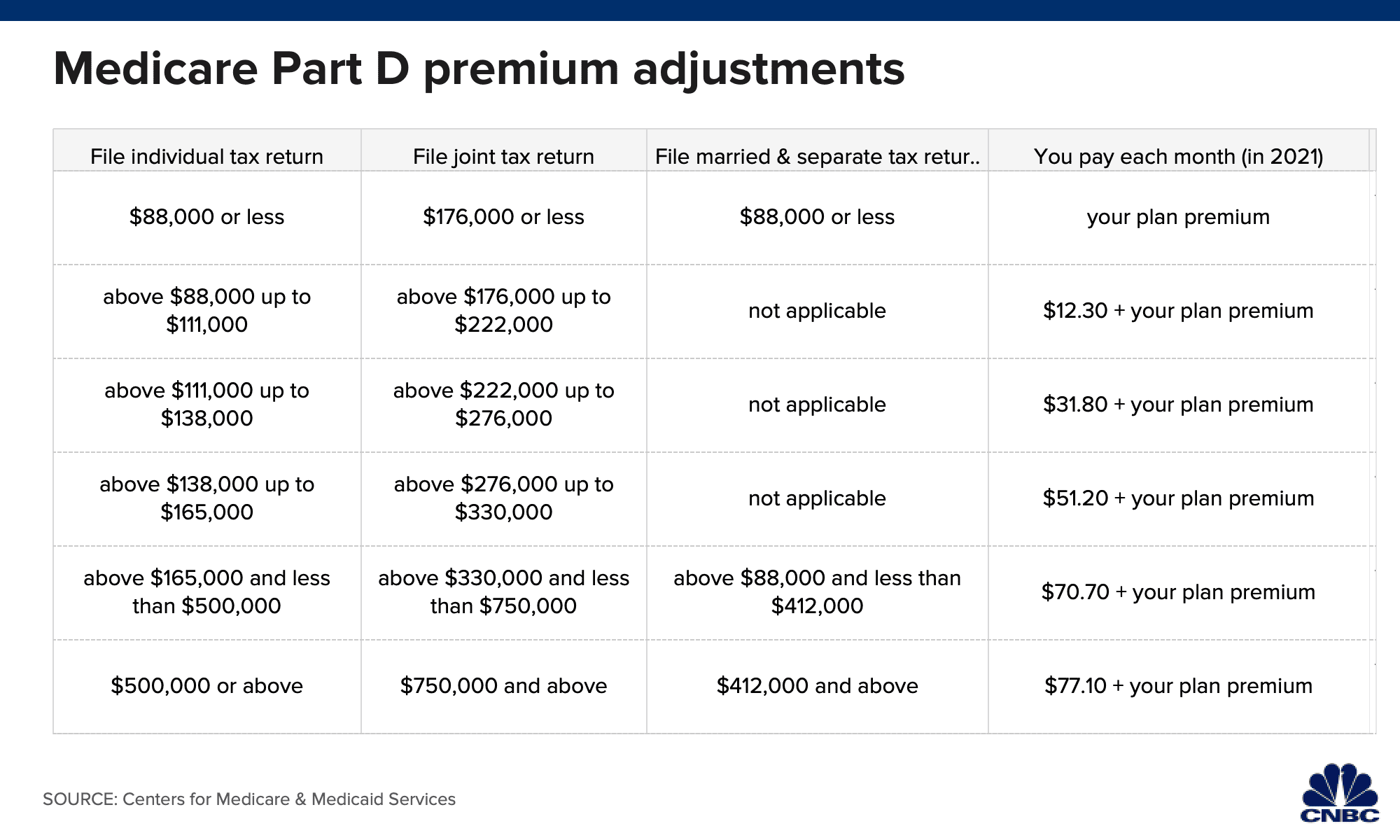

The remaining beneficiaries stick with basic Medicare and may pair it with a so-called Medigap policy and a stand-alone Part D plan. Be aware that higher-income beneficiaries pay more for drug coverage, as well (see chart below).

Remember that late-enrollment penalties last a lifetime. For Part B, that surcharge is 10% for each 12-month period you could have had it but didn’t sign up. For Part D, the penalty is 1% of the base premium ($33.06 in 2021) multiplied by the number of full, uncovered months you didn’t have Part D or creditable coverage.

Working at a large company

The general rule for workers at companies with at least 20 employees is that you can delay signing up for Medicare until you lose your group insurance (i.e., you retire).

Many people with large group health insurance delay Part B but sign up for Part A because it’s free.

“It doesn’t hurt you to have it,” Roberts said.

However, she said, if you happen to have a health savings account paired with a high-deductible health plan through your employer, be aware that you cannot make contributions once you enroll in Medicare, even if only Part A.

Also, if you stay with your current coverage and delay all or parts of Medicare, make sure the plan is considered qualifying coverage for both Parts B and D.

If you’re uncertain whether you need to sign up, it’s worth checking with your human resources department or your insurance carrier.

“I find it is always good to just confirm,” said Elizabeth Gavino, founder of Lewin & Gavino and an independent broker and general agent for Medicare plans.

Some 65-year-olds with younger spouses also might want to keep their group plan. Unlike your company’s option, spouses must qualify on their own for Medicare — either by reaching age 65 or having a disability if younger than that — regardless of your own eligibility.

If your employer is small

If you have health insurance through a company with fewer than 20 employees, you should sign up for Medicare at 65 regardless of whether you stay on the employer plan. If you do choose to remain on it, Medicare is your primary insurance.

However, it may be more cost-effective in this situation to drop the employer coverage and pick up Medigap and a Part D plan — or, alternatively, an Advantage Plan — instead of keeping the work plan as secondary insurance.

Often, workers at small companies pay more in premiums than employees at larger firms.

The average premium for single coverage through employer-sponsored health insurance is $7,470, according to the Kaiser Family Foundation. However, employees contribute an average of $1,243 — or about 17% — with their company covering the remainder.

At small firms, the employee’s share might be far higher. For example, 28% are in a plan that requires them to contribute more than half of the premium for family coverage, compared with 4% of covered workers at large firms.