Is the great value rotation over?

The S&P 500 is at a historic high, but investors who earlier this year overweighted their portfolios into reopening stocks like Caterpillar and banks, and away from tech and other growth stocks, appear to be rethinking that strategy.

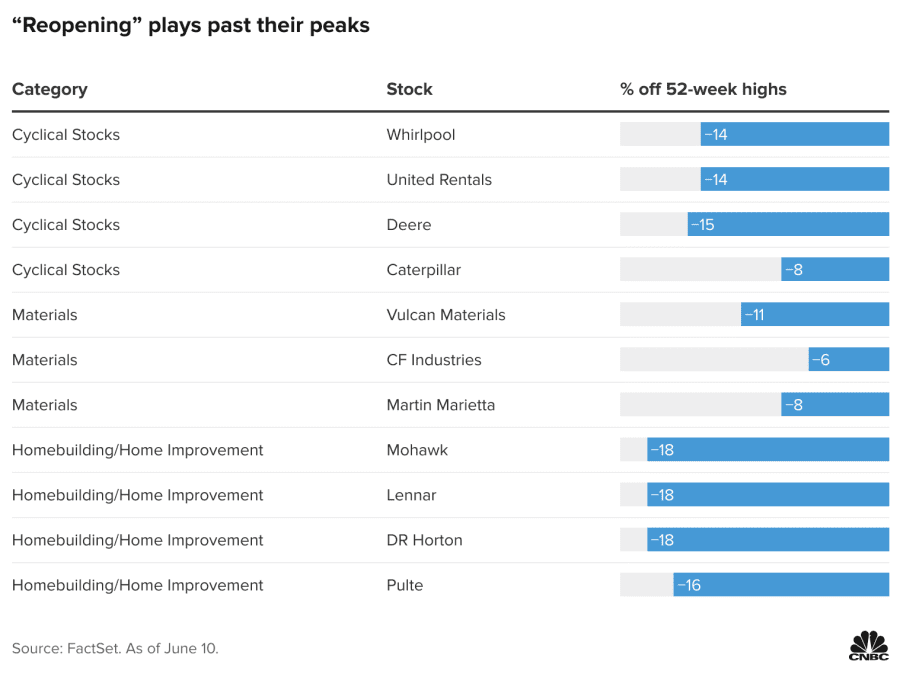

Many of the companies associated with the “reopening” trade topped out in April or early May:

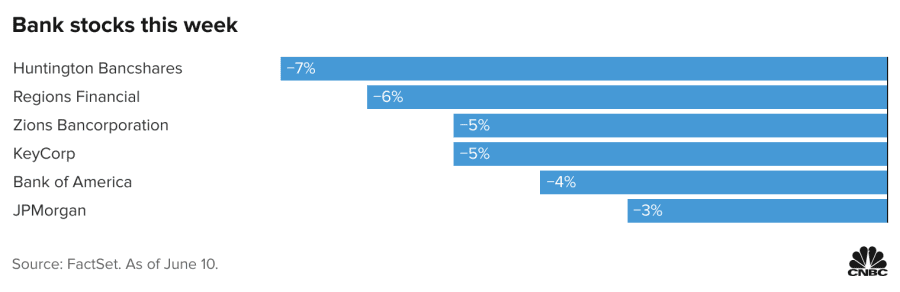

Now, a final leg of the so-called “value” trade is also cracking this week: banks.

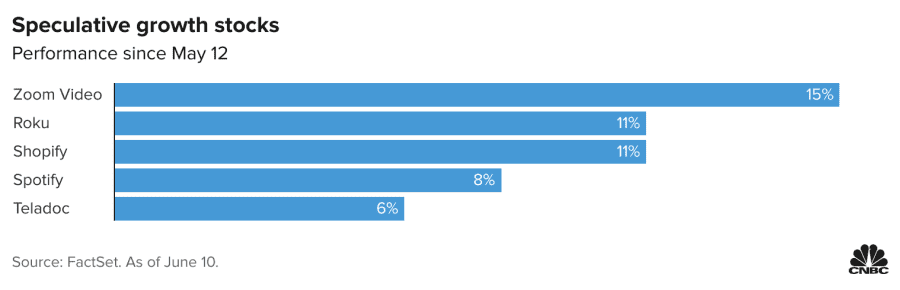

Investors instead have begun rotating back into old-school growth stocks.

Thursday saw new highs in Cisco, Alphabet and IBM. But perhaps more importantly, formerly deeply out-of-favor speculative growth stocks, many of them associated with Cathie Wood’s ARK funds, have begun to rebound.

The changing market narrative

What’s going on?

The market narrative is changing. The first quarter storyline was that the reopening would be very strong, bond yields would move up, and inflation may be an issue later in the year.

This was only partially correct. The reopening has been strong, but bond yields have come down, not up, as investors have come to believe 1) that inflation and supply-chain issues may indeed be “transitory,” or temporary, as the Federal Reserve has insisted, and 2) that the second and third quarter is the top in earnings and economic growth.

“The value trade is unwinding, and the growth bulls are winning,” Alec Young, chief investment officer at Tactical Alpha, told me. “Bond yields are a proxy on the growth outlook,” he added, noting that bond investors see moderating inflation and a slower rate of growth (though still positive) in the second half of the year.

The result: Investors are staying in the market, but they are rotating into defensives (health care) and growth (technology). Formerly crowded trades like cyclicals and banks that are associated with the “value trade” are now retreating.

Why would investors rotate into growth stocks if growth is slowing?

“Value is a more economically sensitive sector because value is weighted toward industrials, energy, materials, and small caps,” Young said.

“Early in the economic cycle, coming out of a recession, there is more earnings leverage from value stocks, so they are a better investment,” he added.

“The problem is that everything has been compressed,” Young said. “We went into a recession really fast, and we came out of it fast, partly due to all the stimulus. Growth stocks now offer more reliable growth and are less subject to the vagaries of the economic cycle.”

In a recent note to clients, Goldman Sachs’ Ben Snider and David Kostin agreed. “History, valuations, positioning, and economic deceleration indicate that most of the rotation [from growth to value] is behind us,” they said.

Because this was a “crowded” (overweight) trade, Goldman suggested that many players are likely caught offsides. “Mutual funds are overweight Value to a larger degree than any time in our eight-year data history,” they said. “Hedge funds remain tilted toward Growth, but that tilt has recently fallen sharply and now ranks as the lowest in over five years.”