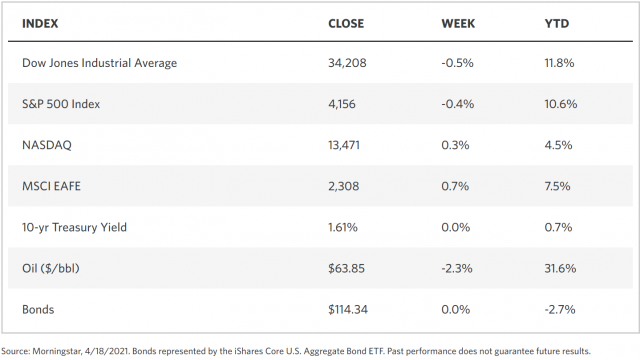

Stock Markets

The stock indices registered mixed outcomes after increased trading volatility the past week. Ending marginally lower is the large-cap S&P 500 Index, while the tech-dominant Nasdaq Composite Index increased slightly. The mixed results indicate that there is a measure of strength and resiliency in the US economy, although concerns are increasing surrounding the inflation rate the whether or not the Federal Reserve might adopt more severe measures to temper the overheating economy. The sector that posted the strongest gain in the S&P 500 is health care, while energy and industrials registered the greatest loss. The issue that affected the markets the most is that of the likelihood of inflationary pressures. The economy is gradually picking up steam while corporations report record profits over the previous year, the rising inflation appears to be less threatening in light of the bigger picture. The stock market’s performance appears to be quite stable and continued growth is expected even in light of the occasional volatility.

U.S. Economy

While concerns about a possible derailment of the ongoing economic recovery are understandable, the broader picture continues to be that of an intact and stable economy. Worries about rising inflation are nothing new in the recent economic milieu, and a rundown of the prior risk factors will provide a sense of how economic indicators will achieve equilibrium in the long run. We might cite the following:

- The 10-year Treasury yield, which is the benchmark for the 10-year interest rates, began 2021 below 1% for the first time in history. It promptly surged from 0.93% to 1.73% by the end of the first quarter. Because of the suddenness of its rise, stock investors were taken by surprise and cause the market to pull back by 4% twice during the same period. We observe that rates may be higher but historically are far from high. The expectations for stronger economic growth which had driven the interest rate increase, coming from a year of economic recession due to the lockdowns, appears to be a factor that will continue to influence the markets in the long term.

- The steep rise in stock prices from the deep market drop in March of last year has brought valuations to their peak in the last two decades, causing investors to worry that a major market correction is impending. In the first year of the recovery, the S&P 500 ascended by 75% as investors priced in their speculations that a strong rebound in corporate profits is imminent. That expectation is materializing, with earnings reports showing a 49% increase for the first quarter of 2021. Prices have increased faster than reported profits, although this is far from resembling the 90’s dot-com bubble or the financial asset crisis of past years because this time around profits are recovering from a deep fall than coming off their peak levels.

Metals and Mining

Gold continues on its upward trend that began towards the end of February, increasing at a rate of 8.9%. The recent strong performance of the 10-year Treasury yields and the U.S. exchange rate that tended to halt the advance of metal prices have decreased in April, providing gold an opportunity to advance further. The drop in yields and the dollar were in turn prompted by the strong inflation push during the week. Aside from improving fundamentals, however, the technicals show an increasing likelihood of an upward trading momentum since investors are of the opinion that the metal has already attained an interim trading low. Gold traded at $1,872.45 per ounce on Friday, May 21.

Silver approached the $30 per ounce resistance level on May 17 at the start of the trading week, but it lacked the momentum to break out. Although silver did not make it past the threshold, the continuation of the trend is likely to keep the metal at its previous highs after a period of moderate gains over the next two years. At some point, silver will gain sufficient strength to break through the barrier, possibly coinciding with the next economic and financial meltdown. The target price may be $50 at that instance. As for this week, silver closed at $27.43 on Friday.

Palladium, on the other hand, reached an all-time high of $2,829 per ounce this week due to tightness in the supply that may stretch throughout the remainder of 2021, further contributing to the rise in price. It might test the $3,000 level for the year, representing an increase of 37% year-on-year. It settled at $2,691.50 per ounce at midday last Friday. Platinum ended the week flat at $1,168 per ounce, declining 4% from Monday.

In the base metals sector, copper continued its consolidation patterns since it ascended to its all-time high at the beginning of this month when it marked its $10,724.50 per tonne resistance level. This week, it corrected to below $10,500. Zinc recorded better performance this week when it exceeded its 35-month peak of $3,063.50 per tonne. Its surge was linked to concerns regarding tax increase on Peruvian and Chilean miners that impacted supply. Zinc settled on Friday at $2,945.50 per tonne. Nickel held at $17,326 on Friday after starting the week at $17,523 per tonne. Lead traded slightly upward, beginning Monday at $2,181,50 per tonne and ending the week at $2,202.50, charting an increase of 11% in its value.

Energy and Oil

Oil is facing its biggest weekly correction since March after it charted three days of major losses. It recovered some lost area on Friday after it followed commodities in a broad sell-off on Friday. The IEA released its Net-Zero report in the middle of the week, announcing that in order to reach net zero, no new oil, gas, and coal projects shall be undertaken. This announcement is likely to have an impact on how investors regard to the future price of oil. The report was not given much credence by Asian players, however. Japanese officials regarded the EIA report as merely one of the suggestions as to how the world may reduce greenhouse gas emissions to zero by 2050, but it is not binding upon Japan which has its own energy policies. Philippine officials likewise considered foregoing any additional investment in fossil fuels a development setback that it will not abide by. The OPEC also reacted, commenting that the mandatory stop to new oil and gas investments post 2021 contrasts dramatically with the conclusions reached by other IEA reports. As such it could be the catalyst for potential instability in the oil markets if the new mandate will be followed by investors.

Natural Gas

In the natural gas industry, Qatar is cornering the market by ramping up liquid natural gas supply and reducing its prices, in effect causing a halt to LNG projects in other areas. The expansion plans of the country are significantly large that Qatar, currently the top LNG producer in the world with the lowest cost, may render other producers insignificant or unnecessary. Qatar took this aggressive move due to the threat posed on it by the US as LNG producer in the past year.

For the report week (Wednesday, May 12 to Wednesday, May 19), natural gas spot prices moved sideways. The Henry Hub spot price dipped from $2,90 per million British thermal units (MMBtu) on May 12 to $2.88/MMBtu on May 19. The price of the New York Mercantile Exchange June 2021 contract remained at the same level for the week at $2,964/MMBtu. The 12-month strip price averaging June 2021 through May 2022 futures contracts increased to $3.025/MMBtu, registering an increase of $0.02/MMBtu.

World Markets

European shares surged on indications that the economy is on the road to recovery as the coronavirus restrictions are gradually lifted. Worries remain, however, about the rise in inflation rates. The pan-European STOXX Europe 600 Index grew 0.43% during the weeks’ trading. The region’s major indices were mixed. The Italian FTSE MIB Index rose slightly, while the French CAC 40 Index and the German Xetra DAX Index remained unchanged. The UK’s FTSE 100 Index receded 0.36% as the British currency gained over the U.S. dollar on the back of strong economic reports. The core eurozone bond yields closed higher on speculations that the European Central Bank will likely slow its bond purchases. UK gilt yields dropped on worries that a new coronavirus strain is spreading, thus potentially delaying the UK economy’s full recovery.

In Japan, the stock exchange ended the trading week higher with the broader TOPIX Index up 1.13% but the narrower Nikkei 223 Index returning 0.83%. The economic data report showed mixed results. Japan’s GDP shrunk more than had been anticipated for the first quarter of the year. On the other hand, export growth for April was strong, together with the manufacturers’ business confidence which rallied to its highest level since May 2018. Falling slightly was the yield on the 10-year Japanese government bond that ended at 0.08%. The yen gained strength to close the trading week at JPY 108.66 to the US dollar. In the meantime, Chinese stocks moved sideways on listless trading. Dropping by 1% was the benchmark Shanghai Composite Index, even as the large-cap CSI 300 Index increased by 0.5% in what appears to be a recovery from the decline of its growth stocks in recent weeks. The yields on Chinese bonds fell in the fixed income market in reaction to the disappointing economic data report for April. The renminbi remained unchanged against the U.S. dollar for the week, keeping the gains it made since early April.

The Week Ahead

Among the important reports to be released in the coming week are the GDP, building permits, and the Core PCE deflator reports.

Key Topics to Watch

- CoreLogic Case-Schiller national home price index (12-month change)

- Consumer confidence index

- New home sales (SAAR)

- Initial jobless claims (regular state program)

- Continuing jobless claims (regular state program)

- GDP revision (seasonally adjusted annual rate)

- Durable goods orders

- Nondefense capital goods, excluding aircraft

- Pending home sales index

- Personal income

- Consumer spending

- Core inflation

- Trade in goods deficit, advance report

- Chicago PMI

- Consumer sentiment index (final)

Markets Index Wrap Up