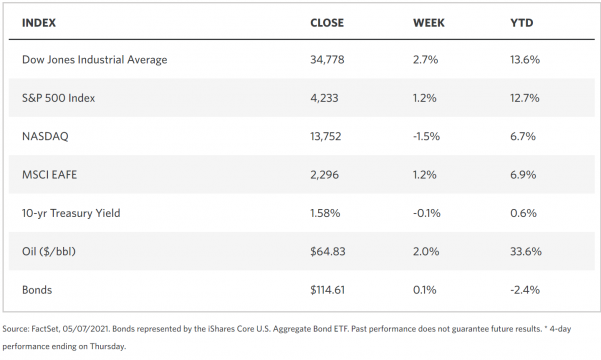

Stock Markets

Stock market indexes ended the week mixed across a broad range of sectors. Volatility set in as losses earlier in the week were partly covered by Friday’s rally. The 30-stock Dow Jones Industrial Average outperformed the technology-dominated Nasdaq Composite Index as the latter charted its heaviest weekly drop in the last eight weeks. The technology sector also underperformed in the broad S&P 500 Index, as did real estate, utilities, and consumer discretionary stocks. Value stocks saw better trading than growth stocks as they did in the previous two weeks. Over the week the earnings season continued to wind down as 442 companies in the S&P 500 listing projected to release their first-quarter performance. Overall, earnings reports have significantly exceeded analysts’ expectations.

U.S. Economy

During the week, the Labor Department released some disappointing job numbers that may have influenced the course of trading during the week. The disappointing jobs report indicated that nonfarm payrolls grew only by 266,000 jobs in April out of the 1 million jobs expected. Despite an increase in jobs in the restaurant and leisure sector, employment in the manufacturing and retail industries was diminished slightly. Overall, the unemployment rate increased slightly from 6.0% to 6.1%, coinciding with a downward adjustment in the March employment figure. The severe shortfall in the expected jobs numbers is a sign that the recovery might not be proceeding as originally forecasted. It also signals a major slowdown in employment recovery compared to the March gain of 770,000 jobs.

- The question posed by the underperformance in the job market is whether or not the shortfall is a firm indication that the economic recovery may not materialize. The analysis shows, however, that the shortfall in jobs created is only a matter of timing rather than a change in trend. The issuance of stimulus checks that were necessary to keep up demands for goods and services has also unfortunately caused a mismatch among employee expectations, with some of the returning employees opting for the stimulus package for the meantime while the opening of establishments is staggered due to covid uncertainties. As the lifting of restrictions continues to accelerate and stimulus payments are eventually discontinued, people will likely move back to their jobs, causing job growth to rise for the rest of the year.

- On the other hand, it is also potentially a positive indication that the anticipated overheating of the economy is unlikely, therefore allaying worries of a runaway inflation rate. There have been concerns that the increase in average hourly earnings, measured at 0.7% month-on-month, is extraordinarily robust and might contribute to some short-term labor shortage. The payroll gains contributed by the leisure and hospitality sector added 331,000 jobs in April, which may be the start in the service-sector jobs comeback. Manufacturing shaved off 18,000 jobs while transportation and warehousing lost 74,000 jobs. The imbalances show a possible mismatch among the industries, which may eventually correct itself as the economy continues to rebound.

Metals and Mining

Gold prices continued on their upward trend, during which it tested and breached the critical $1,800 per ounce level last achieved on February 22 and from which it corrected to $1,735 by the end of the month. Gold prices regained their upward momentum in March as the threat from the advancing 10-year Treasury yields and the strengthening US dollar gradually dissipated, fear over the rising inflation rates intensified, and investors’ flight to gold and other precious metals took off. Gold rose as high as $1,837.70 on Thursday, a surge of 5% from its year-to-date low. It is also up 13% year-over-year in the first quarter of 2021. On Friday, it traded at $1,834.73.

Silver corrected from its February year-to-date high for most of the two months that followed. From its interim low of $25.84 by end of April, it shot up to $27.41 in the past week. It ended Friday at $27.37, close to its recent peak. The fundamentals for silver remain positive and are expected to provide buying impetus for the metal for the rest of the year, on the back of increased investment and industrial demand. Platinum and palladium remain strong due to continued forecasted demand. Platinum prices are up 17% year-to-date, selling at $1,246 per ounce on Friday. Palladium prices remained above $2,000 for most of the past year. Since this metal is a key element of car emission systems, the increasingly robust emission standards in the EU and China are likely to sustain demand and push its prices higher. Palladium traded at $2,837.50 on Friday.

Base metals rode the same bullish market as precious metals. Copper pushed above $10,000 per tonne to test its record high of $10,025 on Thursday. It traded at $10.215 on Friday. Zinc also recorded gains by rising to a year-to-date high at $2,959.50 per tonne by midweek. A pullback occurred later in the day, but the metal rallied to Friday’s price of $2,978.50. Nickel began the week at $16,009 per tonne, but surged a further 12% by Thursday. It still needs a ways to go before coming back to its year-to-date high of $19,689 established on February 22. It aimed to test $17,843 by the week’s end. Lead also gained, attaining its year-to-date high of $2,186 per tonne, ending Friday at $2,177.

Energy and Oil

Brent is testing its resistance at $70 per barrel which it approached on Wednesday, but retreated from on Thursday. Demand is still expected to remain strong, however, as the week still closed with a gain. World trends in fuel sourcing continue to move against the use of fossil fuels, however. A recent report released by the United Nations suggests that the global rise in methane emissions in the past 10 years is attributable mainly to the sudden rise in oil and gas drilling, or more specifically, the shale boom in the U.S. The study optimistically foresees, however, that costs related to reductions in methane are actually inexpensive and within achievable targets. Along the same theme, Germany moves up its climate targets as a court decision ordering tougher action prompted the government to raise its 2030 emissions reduction target from 55% to 65%. The country is also advancing its net-zero target from 2050 to 2045.

Natural Gas

There has been a diminution of the viability of LNG import terminals in Europe, prompting utilities to look for alternative uses. Waning demand for LNG is causing companies to turn to other projects such as switching to a hydrogen hub (Unier SE) or transformation to an offshore wind project in Ireland. Movements of natural gas spot prices were mixed for the week (April 28 to May 5). The Henry Hub spot price increased from $2.93 per million British thermal units (MMBtu) at the start of the week to $2.97/MMBtu by the week’s end. This is a reflection of increasingly variable temperatures across the country. Last Wednesday, the New York Mercantile Exchange (NYMEX) contract expired at $2.925/MMBtu. The June 2021 contract price descended to $2.938/MMBtu, a reduction of $0.02/MMBtu for the week. The price of the 12-month strip averaging June 2021 through May 2022 futures contracts slid to $2.977/MMBtu, a drop of $0.01/MMBtu.

World Markets

European shares ascended on better-than-expected earnings reports and rising investor confidence buoyed by the economic recovery. The pan-European STOXX Europe 600 Index closed the week 1.72% higher, as did the major indexes for the region. German and French stock indexes were lifted by more than 1.5% and Italy’s FTSE MIB Index gained 1.95% over the same period. The UK’s FTSE 100 Index outperformed the others as it rose by 2.29%. The rise in investor sentiment is fueled by the European Commission’s announcement to reopen the EU’s borders once more to tourists from outside the bloc, targeted for sometime in June. Core eurozone bonds slid at the beginning of the week due to the lower-than-expected US manufacturing reports. Overall for the week, however, yields on peripheral eurozone government bonds moved higher.

In Japan, despite a holiday-shortened week, equities at once recorded a gain on reduced concerns about the pandemic. The Nikkei 225 climbed by 1.89% while the broader TOPIX Index matched this increase by a 1.83% gain of its own. The close of the market occurred for the first three trading days in celebration of the Golden Week, which somewhat reduced volatility and limited reactions to the end-of-week gains in other world markets. The improving prospects for global economic recovery and better-than-expected economic data from the US provided investors an incentive to rally the market. The yen remained mostly unchanged against the U.S. dollar at slightly above JPY 109. The yield on the 10-year Japanese government bond dipped slightly to 0.08%

While most global equities were up, Chinese stocks fell also on the back of a shortened trading week. The Shanghai Stock Exchange Composite Index closed lower by 0.8% while the large-cap CSI 300 Index lost ground by 2.5% from the previous Friday. Mainland markets were closed from Monday through Wednesday for the Labor Day holiday, and reopened on Thursday. Consumer stocks outperformed the rest of the market as investors’ buying motivation was fueled by the preliminary data covering holiday sales and travel. Some pharmaceutical companies saw their stock prices descend after the U.S announced a possible waiver of COVID-19 vaccine-related intellectual property rights. This decision is likely to increase competition among several vaccine makers. Meanwhile, the yield of China’s 10-year sovereign bond slid by 3 basis points to 3.17%.

The Week Ahead

During the coming week, vital economic data expected to be released include Retail sales, Inflation data and the Consumer Sentiment Index.

Key Topics to Watch

- NFIB small-business index

- Job openings

- Consumer price index

- Core CPI

- Federal budget

- Initial jobless claims (regular state program)

- Producer price index

- Retail sales

- Retail sales ex-autos

- Import price index

- Industrial production

- Capacity utilization

- Consumer sentiment

- Business inventories

Markets Index Wrap Up