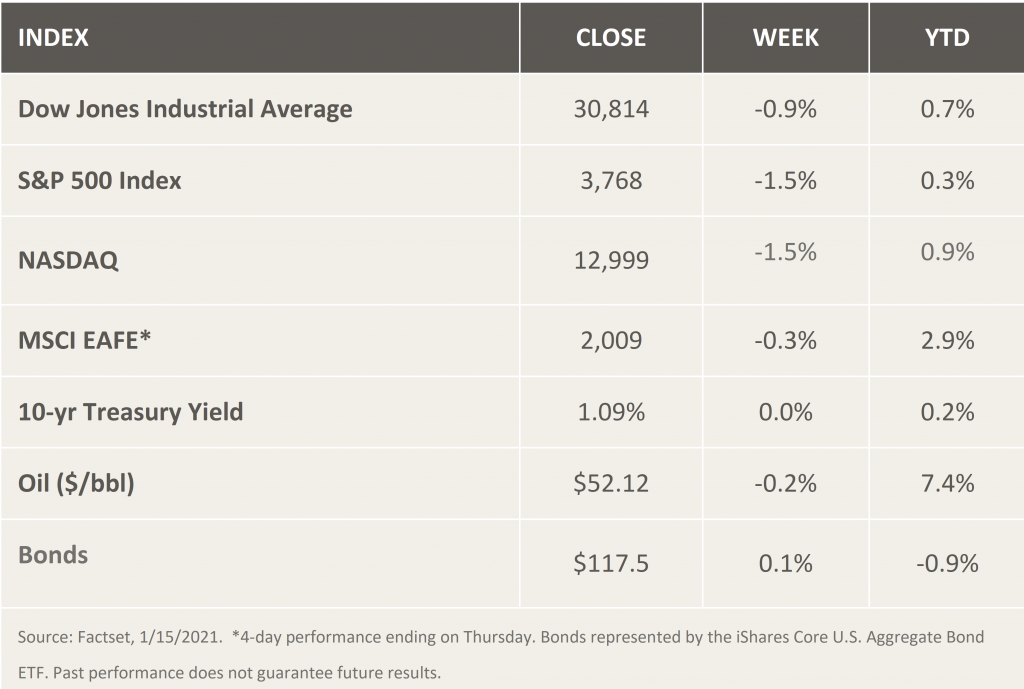

Stock Markets

After hitting record highs in the first trading month of the year, stocks corrected by more than one percent at the close. Earnings reports were released by JP Morgan and Wells Fargo at the start of what analysts anticipate will be a robust earnings season. The much-awaited fiscal-stimulus package was indeed announced by President-elect Joe Biden to the tune of $1.9 trillion, intended to mitigate the COVID-19 impact. Fears of an extended economic lockdown spread among the investing community as the new highly-contagious coronavirus strain appeared over several states and the vaccine roll-out failing to meet expectations. Further need for economic stimulus is signaled by a slowing job market as initial claims spiked during the two weeks ending January 9. The current short-term outlook looks volatile, however, the classic response of the stock market to the coming fiscal and monetary stimulus is expected to be optimistic and would only be further bolstered by resolution of the current delays in vaccine distribution.

U.S. Economy

As the stock market appeared to lose its steam after testing historic highs, fixed income and Treasury yields drew the attention of investors during the first two trading weeks of 2021. Although the benchmark 10-year Treasury yields started the new year at what turned out to be the lowest level to start a new year in history, it has steadily climbed to test the highest level it has been since March before ending Friday on a slight correction. Future potential higher yields for investors poses some interesting prospects:

- Inflation for December increased only slightly, registering a comparatively modest price index gain of 1.6% compared to 2.2% the year before, with the exclusion of energy and food. Expectations for future inflation, though, appears to be trending up for the first time in years, as indicated by the 10-year breakeven rate reaching levels unseen since 2018.

- The announced fiscal stimulus plan amounting to $1.9 trillion represents approximately 9% of GDP. The economic plan covers added relief checks to households, increased unemployment benefits, an expansion of minimum wages, funding for the COVID-19 vaccine, and expanded aid to states and local governments. The increased spending is expected to strengthen recovery efforts while adding to the already growing bond supply and moving yields higher.

- Under a scenario marked by a possible sudden increase in long-term yields, growing inflation, and a resulting tightening of monetary policy by the Fed, valuations may come under pressure resulting in greater market volatility.

In a strong interest rate regime, it is appropriate for investors to allocate a major proportion of their portfolio to bonds and other fixed-income investments. Certain sectors in the equities market will continue to remain viable and attractive such as the technology sector which generally outperforms the market due to strong earnings. Investments that are economically sensitive and that have recently lagged, such as small-cap stocks, can also provide buying incentives.

Metals and Mining

After dropping from a year-to-year high during the week, gold prices recovered to show modest gains on January 15th. It was priced at a 60-day high of $1,942 per ounce on January 4th but gave up its gains on January 11th when it slid 5% to $1,834.70. Nevertheless, analysts expect a further move upward due to the anticipated $1.9 billion stimulus package. Gold is also expected to gain from a possible stock market pullback and inflationary pressures as a result of investors’ flight to safety. By 10:02 am EST on Friday, gold was trading at $1,840.10 per ounce.

Silver continued on a slow uptrend during its second straight week in an attempt to test its five-month-high of $30 per ounce set in early January. Continued volatility has kept the metal below the $26 level for the week, trading at $25.01 at 10:10 a.m. on January 15th. In the meantime, platinum moved closer to its three-year peak of $1,114 per ounce on Thursday, while palladium ticked up slightly. Supply challenges out of South Africa during the year are bound to benefit the prices of both metals, according to analysts. Palladium traded at $2,284 while platinum was priced at $1,075 as of 10:45 p.m. on Friday.

Base metals are mixed for the week, responding to both corrective pressure and buying interest due to concerns that coronavirus lockdowns may disrupt supply chains and cause shortages. Copper prices traded at $7,951 per tonne which represents a 2.3% slide from its January value of $8,146, an eight-year high. It recovered slightly on Friday morning to trade at $8,002The week’s trades saw zinc at $2.716 and lead at $2,040, while nickel rose 4.5% due to supply disruptions from the Philippines, the world’s second-largest nickel exporter.

Energy and Oil

Market sentiments weighed heavily on oil prices as China reported its highest COVID-19 case count in months. OPEC upgraded its forecast for U.S. oil production to increase by 370,000 bpd from a previous expected 71,000 bpd. Total decides to withdraw from the American Petroleum Institute, the most powerful lobby in the industry due to API’s opposition to methane regulations, EV subsidies, and carbon pricing. Total likewise took issue with API’s political contributions to U.S, politicians who oppose the Paris Climate Agreement. In related developments, Saudi Arabia has announced a reduction in its sales of oil to 11 or more Asian refineries, in compliance with its commitment to reduce oil production by 1 mb/d.

Regarding renewables, companies in the solar and wind power industries rose in value, prompting the likelihood of a growing bubble in clean tech stocks. Major investments in clean energy are also foreseen in a possible sequel package to Biden’s stimulus plan, which ay likely to take place in the spring. It bears watching whether the rally in clean energy will remain sustainable in the long term.

Natural Gas

Skyrocketing LNG prices due to seasonally cold weather have expanded beyond Asia to other regions of the world. Consumers are being forced to cut back Global markets are experiencing consumer cutbacks due to supply shortages, further undermining the spot market and possibly driving players to seek greater stability through oil-linked contracts. In Mozambique, a chronic insurgency poses risks to Total’s $23 billion gas production and LNG export project, which halted work due to nearby attacks. The same situation poses risks to ExxonMobil’s planned $33 billion facility. Finally, the Port of Cork in Ireland allowed its agreement with NextDecade Corporation for an LNG import terminal to expire due to concerns surrounding methane emissions. While NextDecade has been experiencing setbacks for similar projects in Europe it still is currently in plans for an LNG export terminal in Texas.

World Markets

A resurgence in coronavirus outbreaks in Europe tempered optimism in a prospective Biden stimulus package. The pan-European STOXX Europe 600 Index slid 0.81% lower; the German Xetra DAX Index declined by 1.86%, Italy’s FTSE MIB by 1.81%, and the French CAC 40 by 1.67%. The UK’s FTSE 100 Index lost 2.00% in response to economic data indicating that its economy contracted in November as a result of a more stringent coronavirus lockdown. Political uncertainty in Italy prompted cored eurozone government bond yields to fall and peripheral eurozone bond yields to climb. UK gilt yields rose for the first half of the week but gave back their gains in the second half to end down overall due to coronavirus concerns, mirroring trading patterns in core markets.

Shifting focus to the Asian markets, Japan’s Nikkei 225 Stock Average surged 380 points (1.4%) to end at 28,519.18, a new decades-long record weekly closing high, The large-cap TOPIX Index moved sideways while the TOPIX Small Index descended. The resiliency of Japan’s markets can be attributed to loosened government lending policies and financial support during the pandemic. Chinese stocks gave up their gains as nine other Chinese companies were added to the U.S. investment blacklist on Thursday, bringing the total of blacklisted companies to 44. These companies were cited for their ties to the Chinese military. The large-cap CSI 300 Index slid by 1.4% while the Shanghai Stock Exchange Composite Index fell by 0.6%, on jitters that Alibaba and Tencent might likewise be blacklisted. Further disappointing news surrounded Sinovac’s coronavirus vaccine CoronaVac, which was found by Brazilian scientists to barely exceed 50% efficacy, far below initially reported levels.

Brazil’s Bovespa Index descended 3.7% on news that the country’s 2020 inflation was 4.5%, a four-year high, with core inflation likely to extend to 5% by midyear due to price shocks in the food and electricity sectors. Turkey’s BIST-100 Index also declined, by about 1% due to a reported current account deficit of $35 billion from January to November 2020.

The Week Ahead

Monday is Martin Luther King Day in recognition of which markets will remain closed. For the rest of the week, economic data to be released will include building permits, housing starts, existing home sales, and PMI breakdowns.

Key Topics to Watch

- National Association of Home Builders

- Inauguration of Joe Biden as president

- Initial jobless claims (state program, SA)

- Continuing jobless claims (state program, SA)

- Housing starts

- Building permits

- Philadelphia Fed Index

- Markit manufacturing PMI

- Markit services PMI

- Existing home sales

Markets Index Wrap Up