We are still in the earliest days of the new decade, one sure to bring with it a plethora of changes. Some we can already foresee happening, while others remain unknowable to us.

One certainty which will forever remain, though, involves investors’ hard-earned cash. Namely, everybody will always want to know where the best opportunities for ample returns lay.

So, how to find out, then? As is de rigueur in the investment fraternity, the new year comes along with recommendation lists. Joining the fray is California based investment firm, Roth Capital. The company is adept at unearthing untapped potential with its primary focus on small-caps.

We decided to get the scoop on 5 companies the investment firm thinks stand to make headway in 2020. All choices, according to the analysts, have room for solid upside, and, additionally, all currently hold a Strong Buy consensus rating from the Street. Here’s the lowdown.

PowerFleet Inc (PWFL)

Let’s start with one of Roth’s choices in the technology sector. Formerly known as I.D. Systems, PowerFleet is a pioneer in the use of radio frequency identification (RFID) technology for industrial asset tracking and management. With its patented systems for managing high value assets, the company serves big industry names such as Ford and Avis, as well as the U.S. Postal Service.

The company’s latest earnings report achieved record quarterly revenue of $16.9 million, representing a year-over-year increase of 26%. The quarter also saw the company sign a number of deals with major players such as Knight-Swift, The Scotts Miracle-Gro Company, B.A.H. Express and Jungheinrich.

In October PowerFleet completed the acquisition of Israeli based Pointer Telocation, a leading provider of telematics and mobile IoT solutions, for approximately $140 million. Roth’s William Gibson views “the combination as transformational, positioning the company for additional and larger orders.”

“Our 2020 estimate is in line with guidance, earnings of $7.6 million or $0.26 per share on revenue of $153 million. Cross-selling opportunities are well underway and should result in meaningful upside to guidance,” the analyst said.

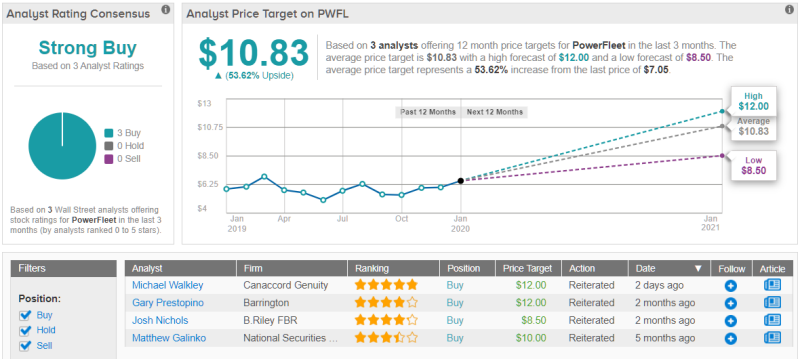

Gibson, therefore, reiterated a Buy rating on PWFL, and kept his price target of $10.30 intact. Should the objective play out, gains of 46% could be heading investors’ way over the next 12 months.

2 other analysts are currently tracking the asset tracker, with both recommending the stock a Buy. PowerFleet’s Strong Buy consensus rating is accompanied by an average price target of $10.83 and represents possible upside of 54%. (See PowerFleet stock analysis on TipRanks)

Forty Seven Inc (FTSV)

Moving on to the healthcare sector, we encounter Forty Seven Inc. The biotech is engaged in finding novel and more compassionate ways to fight cancer. FTSV has been turning heads on the Street recently, as December saw a tripling of its share price.

The reason? Last month, Forty Seven announced promising updated clinical data from its ongoing phase Ib trial evaluating Magrolimab in combination with Azacitidine for the treatment of myelodysplastic syndrome (MDS) and acute myeloid leukemia (AML).

The combination of Magrolimab and Azacitidine proved to be highly active and well-tolerated in patients with MDS and AML. Magrolimab is a humanized monoclonal antibody targeting CD47, which is a “don’t eat me” signal to macrophages and is expressed on all cells.

After such a mercurial run up, what might move the stock even further?

Roth’s Anthony Butler thinks It could be “inferences of magrolimab’s utility in solid tumors.” The 4-star analyst further expounded, “While we do not know the data, an early Phase Ib trial of magrolimab plus cetuximab in colorectal cancer will be presented at the Gastrointestinal Cancers Symposium (ASCO-GI) January 23-25 in San Francisco and as well as magrolimab plus avelumab in ovarian cancer at ASCO-SITC Clinical Immuno-Oncology Symposium February 6-8 in Orlando. The trials could possibly provide an early read on the utility of magrolimab in solid tumors. Any positive data most likely will increase the value of the stock.”

Butler confirmed his bullish take on Forty Seven by reiterating a Buy rating on the cancer fighter. The analyst’s price target is $55 and implies upside potential of 56%.

It looks like the rest of the Street unanimously agrees with the Roth analyst. A Strong Buy consensus rating is formed of solely Buy ratings – 9, in fact. 13% upside could be in the cards should the average price target of $41.75 be achieved over the coming 12 months. (See Forty Seven stock analysis on TipRanks)

NV5 Holdings (NVEE)

NV5 Holdings suffered badly in the bull market of 2019, losing almost 17% of its value over the year. A series of disappointing earnings reports hampered the stock’s growth potential. The infrastructure-focused engineering and consulting company has started the new decade well, though, and is so far up by over 10% year-to-date.

NV5 have been busy on the acquisition front; In December, the company completed the purchase of Geospatial Holdings (QSI), the US’s largest independent geospatial analytics firm for approximately $318 million. The acquisition was the company’s 7th in 2019 alone.

Roth’s Jeff Martin thinks a turnaround is due and foresees the trend extending further into 2020. The 5-star analyst said, “We chose NVEE as the top pick for Business Services in anticipation of the improved margin profile of the business in 2020. We model a 420bp improvement in adjusted EBITDA margin (on net revenue) to 21.2%, aided by the 24% margin from the QSI acquisition. QSI also brings organic growth potential and continued strength in NVEE’s Energy group aid in the return to organic growth in 2020.”

Martin, accordingly, reiterated a Buy rating on NV5, along with a price target of $91. This implies upside potential of a not inconsiderable 63.5%.

Overall, those keeping an eye on NVEE stock remain with the bulls. NV5’s 3 Buy ratings coalesce into a Strong Buy consensus rating and come accompanied with an average price target of $87.33. The figure indicates upside potential of over 60% upside. (See NV5 stock analysis on TipRanks)

Aspen Group Inc (ASPU)

Combining tech with education, Aspen group has two for-profit universities under its holdings umbrella, Aspen University and United States University. The company provides online degrees along with on-campus studies.

ASPU’s innovative monthly payment plan allows students to pursue degrees without the burden of student loans, while the university’s option to pay in monthly increments provides the ability to pay for education in significantly lower amounts. Aspen has been posting impressive growth figures in its latest earnings report, exhibiting 49% year-over-year growth, while also reporting record revenue of $12.1 million.

Roth’s Darren Aftahi anticipates “continued topline growth (~36% y/y NTM) to be driven by further expansion of ASPU’s two higher growth and profit segments, USU and Pre-Licensure (PL).” The 5-star analyst further added, “We expect variable enrollment costs to be kept stable as ASPU should continue to benefit from its industry differentiating EdTech enrollment CRM (and with it double-digit conversion rates), suggesting continued leverage in marketing costs y/y, while maintaining double-digit enrollment growth (with upside in 2H20 from the launch of 2 additional PL campuses). Shares remain attractive trading at <2.5x FY21 revenue on ~30% y/y growth and runway for incremental profitability in the NTM.”

Unsurprisingly, then, Aftahi kept his Buy rating on ASPU, along with his price target of $11. The figure indicates potential upside of 40%.

When put together, Aspen’s 4 Buy recommendations from the Street add up to a Strong Buy consensus rating. An average price target of $10.75 indicates possible gains of 36%. (See Aspen stock analysis on TipRanks)

CryoPort Inc (CYRX)

With Roth’s final pick we head back to the tech sector. Cryoport provide logistic solutions for the life sciences industry. Specifically, the company deals in the global transportation of temperature-sensitive materials and serves biopharmaceutical, IVF and surrogacy and animal health organizations around the world.

The company is growing rapidly and making its way towards profitability. In 3Q19 revenues were up by 81% year-over-year with reported record revenue of $9.6 million. The company is expected to start turning a profit in 2021.

After CYRX’s share price rose by over 150% in 2019’s first eight months, the final months of the year saw it experience a pullback. Roth’s Richard Baldry, though, sees the retracement as an opportunity. The 5-star analyst picks Cryoport’s as his “top Software sector pick for 2020.” Baldry said, “As CYRX’s clinical trial customer base increases and commercial therapies supported expand, we expect rapid growth and record revenue and earnings results in 2020, at odds with the roughly 40% pullback in its shares from recent highs.”

To this end, Baldry reiterated a Buy on Cryoport, alongside a price target of $30. Should the target be met, investors stand to take home an increase in the shape of 75%.

CYRX’s fans on the Street are few, yet vocal. Of the remaining 2 analysts chiming in with an opinion on the logistics company, both consider Cryoport a Buy. Therefore, Cryoport receives Strong Buy status. With an average price target of $23.67, the upside potential comes in at 38%.