Stock Markets

As expected, U.S. stocks rallied to fresh record highs after the three main issues that have created most of the uncertainty this year came to a positive close. The trade deal, Brexit and the Fed policy all moved to new positive levels. The U.S. and China reached a “phase one” trade deal which eased fears of further trade issues and offers positive sentiment on the “Phase Two” talks. The agreement includes important items focused on agricultural purchases and offers significant relief from certain tariffs. For the on again off again Brexit, U.K. prime minister Boris Johnson got a positive mandate when his party won a majority in the general election held this week. That will serve to reduce a lot of lingering political uncertainty now that the country plans to negotiate its exit from the European Union. Importantly, the Federal Reserve (Fed) went with its better judgement last week and left interest rates unchanged. That also sent signs of a pause through the coming year for Fed rates. Low inflation gives the Fed flexibility, analysts say, to remain accommodative for the foreseeable future without having to raise interest rates.

U.S. Economy

The immediate enthusiasm over the “phase one” trade deal might have been dampened a bit by some negative economic data released late in the week. The Commerce Department announced Friday that retail sales excluding the auto sector rose only about 0.1% in November. That’s well below the expectations of most analysts. At the same time spending at restaurants, bars, and clothing stores dropped which indicated that consumers may be getting more cautious about discretionary spending. The weekly jobless claims also moved to the highest level in over two years. However, some seasonal adjustments as a result of the really late Thanksgiving holiday may have been the main contributor.

The reports of a preliminary trade agreement resulted created a bounce in Treasury yields on Thursday. Those yields then fell back Friday and ended the week lower as investors seemed to react to the weaker than expected retail sales data. Many traders reported that it was a fairly quiet week in the investment-grade corporate bond market, as investors’ focus on trade talks and somewhat limited year-end liquidity led to subdued risk appetite.

Metals and Mining

Word of a US-China trade deal left the gold price relatively flat on Friday. The relief from uncertainty and avoiding a new round of US tariffs sent investors mostly away gold opting instead for riskier assets. The first phase of a deal between the US and China was set to be completed in November but was given a new deadline of December 15 when it the two powers realized that they would not be reaching on an agreement that would mutually benefit both sides. Gold has been largely supported by the trade war that helped the metal gain over 15 percent in 2019 to date. The dispute between two of the world’s largest economies has caused turmoil in the markets and had investors concerned over a global economic slowdown. Gold was given a small lift when the US Federal Reserve decided to hold steady on the interest rate of 1.5 to 1.75 percent. Silver was also held tight on Friday but managed to make gains over the week. Its safe haven appeal declined, but even so, it landed its best week since late October with a gain just over 2 percent. In terms of the other precious metals, platinum was flat on Friday, but also had what amounted to its best week since late August. The metal rose over 5 percent. FocusEconomics believes that prices are likely to pick up slightly on the back of a fall in global supply. Weak automotive demand resulting from a shift away from diesel vehicles in the European Union is being blamed for capping Platinum’s gains. Palladium was once again the only precious metal to make gains on Friday. Its gain was large enough to push the metal over US$1,900 per ounce for the first time. That took place on Tuesday when a major power outage in South Africa stopped production at several mines increasing concerns over supplies. Palladium metal has risen over 40 percent since the beginning of 2019 with its large gains based on stricter environmental regulations around car emissions.

Energy and Oil

The big energy news this week surrounded the state-controlled Saudi Arabian Oil Company, commonly known as Aramco. The company raised $25.6 billion this week in the world’s largest initial public offering (IPO). Local demand for shares appeared to be strong, however international investors seemed a bit skeptical of the lofty price that the company set for the offering relative to peers in the oil patch. The size of the IPO, which is meant to represent 1.5% of Aramco’s shares, broke the record set by Chinese internet company Alibaba in 2014. The offering puts the value of the internationally integrated oil and gas company at $1.7 trillion. That makes Aramco worth more than either tech giant Apple or Microsoft. Natural gas spot price movements were mixed this week). The Henry Hub spot price fell from $2.37 per million British thermal units (MMBtu) last week to $2.26/MMBtu this week. At the New York Mercantile Exchange (Nymex), the price of the January 2020 contract decreased 16¢, from $2.399/MMBtu last week to $2.243/MMBtu this week. The price of the 12-month strip averaging January 2020 through December 2020 futures contracts declined 6¢/MMBtu to $2.274/MMBtu.

World Markets

Stocks in Europe rose as the U.S. and China drew closer to a limited trade deal, and fears of a disorderly Brexit waned after a crushing general election victory for Prime Minister Boris Johnson and his Conservative Party. The pan-European STOXX Europe 600 Index ended the week 1.05% higher, Germany’s DAX index gained 0.73%, and the UK’s FTSE 100 Index rose 2.11%. The news that the ruling Conservatives won a landslide general election victory was well received. The Tories won 364 of the 650 seats, achieving a majority of 79 seats which is the party’s largest majority since 1987. The pound sterling soared to more than USD $1.35. That’s its highest level since May 2018. Brussels expressed relief over Johnson’s win, but UK traders were skeptical that an accord would be struck by the end of 2020. Others fully expect Parliament to approve the timetable for the Withdrawal Agreement Bill.

In China, stocks surged for the second straight week based on momentum from the “phase one” trade deal, staving off the imposition of fresh U.S. tariffs on nearly $160 billion of Chinese goods that were set to kick in over the weekend. The benchmark Shanghai Composite Index was up 1.91%, and the large-cap CSI 300 Index grew 1.69%. China’s yuan hit its highest level against the U.S. dollar in nearly four-and-a half months. Clearly traders anticipated that the latest agreement would start a softening in a trade war that has constantly weighed on public sentiment this year.

The Week Ahead

In the run up to the Christmas holiday week, there are a number of important economic indicators scheduled for release this week, including industrial production, housing starts, job openings, leading indicators, and on Friday the key numbers for consumer sentiment.

Key Topics to Watch

- Empire state index

- Markit manufacturing PMI (flash)

- Markit services PMI (flash)

- Homebuilders index

- Housing starts Nov.

- Building permits

- Industrial production

- Capacity utilization

- Job openings

- Weekly jobless claims

- Philly Fed

- Existing home sales

- Leading economic indicators

- GDP revision

- Personal income

- Consumer spending

- Core inflation

- Consumer sentiment index

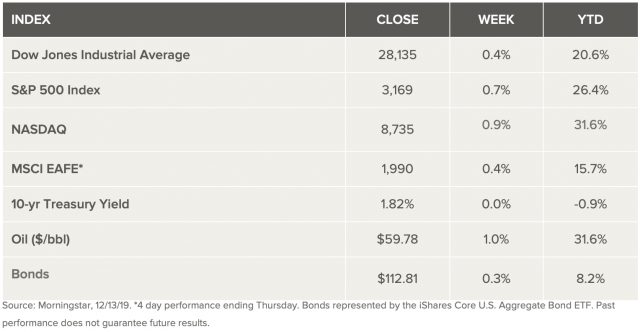

Markets Index Wrap Up