Glenn Daily, age 65, may have found the golden goose.

He’s sitting on a pot of cash that not only accrues interest; it can also be tapped tax-free.

The New York-based fee-only insurance consultant has held onto an insurance policy that his parents first purchased for him when he was just 12 years old. Each year, he pays $253 to keep it in force.

It’s known as a whole life contract — it requires him to pay fixed premiums and offers a tax-deferred interest-bearing account, known as cash value.

For now, the cash value of the policy is about $32,000 and grows at a rate of about 4 percent.

“If you think of this as a fixed income investment, where can I get that?” asked Daily. “Banks are proud to advertise 2 percent on a CD, and here I am getting more than 4 percent.”

He has also tapped that cash in the form of a $27,000 loan, which he has taken free of taxes at an interest rate of 3.7 percent. Daily pays the interest every year and intends on repaying the debt.

Done properly, a tax-free loan on life insurance can offer investors a source of liquidity and tax-free income in retirement.

Done incorrectly, that lifeline can trigger a tax landmine and destroy the insurance policy altogether.

Here’s what you should know about taking a tax-free loan from cash value policies.

Term or permanent

While term insurance covers you for a limited period of, let’s say, 10 or 20 years, so-called permanent life insurance tends to be the tool of choice to protect your heirs from estate taxes.

That’s because the coverage remains in place as long as you keep paying the premiums and the death benefit is generally paid out free of taxes.

Permanent life insurance also includes a cash value savings account, which can grow in a range of different ways, depending on the policy.

Whole life offers a cash value account that grows at a guaranteed rate of interest that’s set by the insurance company. Some insurers pay a dividend, which clients can use to purchase additional coverage. Customers pay a fixed premium for the duration of the policy.

Universal life also has a cash value account that grows based on a minimum interest crediting rate that’s established by the company. If the insurer’s own underlying investments fare well, the company may pay additional interest toward your cash value.

Customers pay flexible premiums with universal life insurance, which means that you may be able to skip premium payments as long as your cash value is sufficient to cover the policy’s costs. Companies also offer different varieties of universal life, sometimes pegging the cash value’s growth to an index, for instance.

Variable life links the growth of your cash value to underlying investments known as subaccounts. These subaccounts are similar to mutual funds and you can decide how to invest.

Expect to pay more than you would for simple term insurance in order to obtain permanent coverage.

A healthy 50-year-old man may pay $21,483 per year for a whole life insurance policy with $1 million in death benefits, according to NerdWallet.

He would pay $1,692 annually for a 20-year term policy with the same death benefit, the personal finance website found.

Tax-free strategy

Here’s how the strategy works:

If you were to withdraw cash from your policy up to the amount you had originally invested, you would receive it free of taxes, but any earnings that are taken out may be subject to income taxes.

That’s why loans are attractive: If you borrow, you use the policy as collateral and take a tax-free loan from the cash value.

“I don’t see it as a primary investment that you should put all of your funds into,” said Jason Wellmann, head of distribution for life insurance at Allianz Life. The insurer offers indexed universal life insurance policies.

“Rather it’s a complement, whether it’s retirement or emergency funding,” he said.

Also, the interest rate for repayment is generally low — 3.7 percent in Daily’s case — when compared with the 10 percent plus you’ll find on a three-year personal loan or the 17 percent interest rate you’ll get on a credit card.

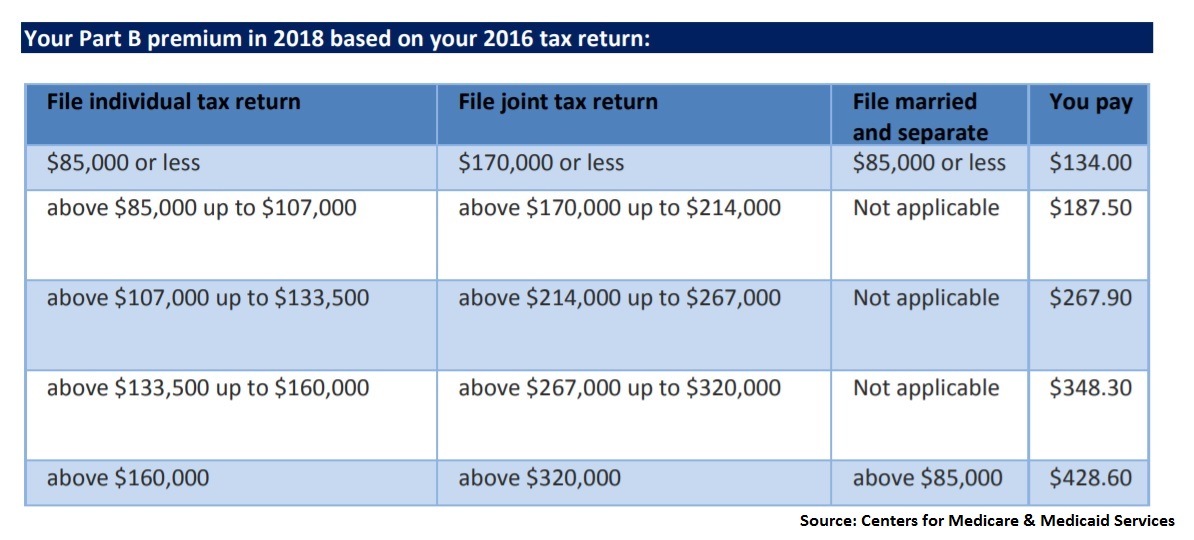

Money from your cash value won’t bump you into a higher income bracket, and you can continue paying the current premium of $134 a month for Part B.

“It’s a great tool for unexpected expenses,” said Tom Love, vice president of insurance analytics at ValMark Financial Group. “If you used a 401(k) for those costs, you would incur income taxes and you can have tax bracket creep.”

But be aware that borrowing — especially if you take regular loans without repaying them — can also go wrong.

Tax trap

Policy loans become problematic when individuals borrow so much they can’t afford to pay the premiums and loan interest.

At the same time, if an over-stretched borrower ceased paying premiums and allowed the policy to lapse, he would get a tax bill, too.

For instance: Your policy has $100,000 in cash value. You have paid $50,000 in premiums, which is your cost basis.

If you allow the policy to lapse, you end up owing income taxes on your gain of $50,000 — the difference between the cash value and your original investment.

“You can accumulate loans so great that they cannibalize the policy and you’re in a ‘damned if you do, damned if you don’t situation,” said Scott Witt, founder of Witt Actuarial Services.

MEC attack

Another potential risk with tax consequences is when your policy has inadvertently become what’s called a modified endowment contract, or MEC.

This means that you have paid in premiums too rapidly, which could happen if you’re trying to beef up your cash value quickly.

While a modified endowment contract still pays a tax-free death benefit, you are subject to income taxes on any policy gains if you take loans or withdrawals.

If you’re under age 59½ when you start taking distributions from a MEC, you also get slapped with a 10 percent penalty.

In order to avoid having your policy considered a MEC, it must meet the “seven-pay test” set by the IRS. The test determines the amount of level annual premiums you would need in order have your policy fully paid up within seven years.

Here’s an example: You have a $100,000 universal life insurance policy with flexible premiums. The MEC limit for the policy is $2,000 a year for the first seven years.

If you decide to pay more in premium during one of those years, then your policy has become a MEC and you face the new tax treatment on loans and withdrawals.

The good news is that your insurer will typically notify you if it receives a payment that may bump you into MEC territory.

Once your policy becomes a MEC, there’s no going back: Even reducing your premium in a subsequent year won’t revert the classification.

The right way

Avoid purchasing cash value life insurance for the express purpose of drawing it down in retirement, advisors said.

“When I buy my permanent life insurance policy, if I ever need it I could use it in retirement, but you should never buy it for that purpose,” said Brett Danko, a certified financial planner and founder of Main Street Financial Solutions in Newtown, Pennsylvania.

“The key is to only buy life insurance when you need it,” he said.

If you already own this type of policy, be sure to revisit it with your financial advisor to check on your cash value and make sure that its performance is on track.

Review your policy annually if you have a pending loan, said Love of ValMark.

Above all, know that cash value life insurance can complement other components of your retirement savings — including your 401(k), IRAs and other accounts — but it should never make up the lion’s share of your wealth.

“There are people who will try to convince you to put all of your money into these policies,” said Love. “Those people are just idiots.”